Cash flow problems rarely start with a dramatic moment. More often, they creep in quietly, an invoice that takes longer to get paid, an unexpected expense, or a few slow weeks of sales. Suddenly, a business that looks healthy on paper is struggling to cover payroll, pay suppliers, or keep up with everyday expenses. Even profitable companies can run into serious trouble when there simply isn’t enough cash available at the right time.

The good news is that cash flow issues are usually manageable when they are identified early and addressed with the right strategies. By understanding the causes, recognizing the warning signs, and taking practical steps to stabilize finances, businesses can regain control without shutting down operations.

In the sections ahead, we’ll break down what cash flow problems actually look like in a business, why they tend to happen, and what you can do to fix them. We’ll also look at how to identify the type of cash flow challenge you’re facing so you can take practical steps to stabilize your finances and keep your business moving forward.

Key Takeaways

- Cash flow problems occur when a business doesn’t have enough available cash to cover expenses.

- Late payments, high operating costs, and rapid growth are common triggers.

- Identifying the type of cash flow problem helps determine the best solution.

- Accelerating payments and controlling expenses can improve liquidity quickly.

- Long-term cash flow management and forecasting help prevent future issues.

What Are Cash Flow Problems?

Cash flow problems occur when a business does not have enough available cash to meet its immediate financial obligations. This situation can arise even if the company is technically profitable. For example, a business might have strong sales and outstanding invoices, but if customers haven’t paid yet, there may not be enough cash available to cover payroll, rent, or supplier payments.

The root of most cash flow issues is timing. Businesses often incur expenses before they receive payment for their products or services. When that timing gap becomes too large, financial pressure builds quickly. Over time, persistent cash shortages can disrupt operations, strain relationships with suppliers, and limit the company’s ability to invest in growth.

Understanding what cash flow problems look like is the first step toward solving them. Once business owners recognize the patterns that cause these challenges, they can begin implementing strategies to stabilize their finances.

What Causes Cash Flow Problems in a Business?

To understand what’s creating cash flow pressure, it helps to look at two areas of the business. Some problems are operational, meaning they arise from everyday activities like invoicing customers, managing inventory, or paying routine expenses. Others are more strategic and relate to decisions around pricing, growth, or financial planning. Identifying which category a challenge falls into can make it much easier to address the root cause.

Operational Causes

One of the most common causes of cash flow problems is slow-paying customers. When invoices remain unpaid for long periods, businesses may struggle to cover their expenses even if they have strong sales. Weak invoicing processes or inconsistent follow-ups can make this situation worse by allowing overdue payments to accumulate.

Inventory management can also create cash flow pressure. When businesses purchase more inventory than they need, a large portion of their cash becomes tied up in unsold products. At the same time, high fixed expenses, such as payroll, rent, and software subscriptions, can quickly drain available cash during slower periods.

Strategic Causes Businesses Often Miss

Some causes of cash flow problems are less obvious. Pricing strategies, for example, can play a major role. If prices are too low or margins are too thin, a business may struggle to generate enough cash from each sale to cover operating costs.

Rapid growth can also strain working capital. Expanding operations often requires spending money on inventory, hiring, and marketing before new revenue arrives. Similarly, offering long payment terms to customers shifts the financing burden onto the business itself. Without proper forecasting, these decisions can create financial pressure even in otherwise successful companies.

In many cases, more than one of these factors may be affecting a business at the same time. That’s why it’s important not only to understand the possible causes of cash flow problems, but also to determine the type of cash flow challenge you’re dealing with. Identifying whether the issue is temporary, structural, or tied to growth can make it much easier to choose the right solution.

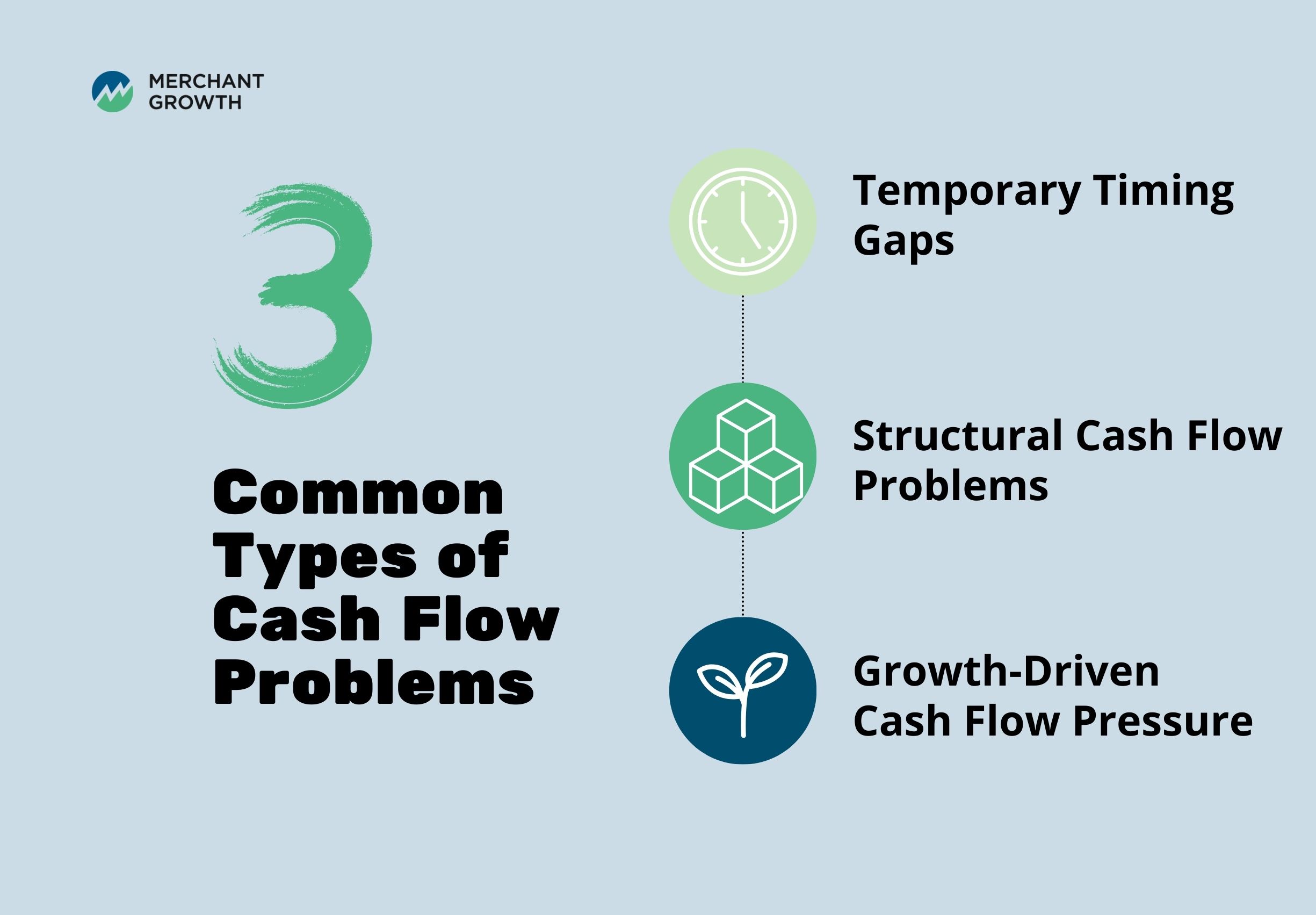

Diagnose the Type of Cash Flow Problem You’re Facing

While these causes can affect businesses in different ways, the impact they have on cash flow isn’t always the same. In some cases the pressure is temporary and tied to timing issues, while in others it reflects deeper financial imbalances or rapid growth. Understanding how the problem is showing up in your business can help clarify what kind of solution is needed.

Temporary Timing Gaps

A temporary timing gap occurs when revenue is coming in, but expenses arrive sooner than expected. This is common when customers take longer to pay invoices or when sales fluctuate seasonally. In these situations, the business may simply need better payment terms or improved collections processes.

Structural Cash Flow Problems

A structural cash flow problem is more serious. In this case, operating expenses consistently exceed incoming cash. This may be caused by high overhead costs, poor pricing strategies, or inefficient operations. Solving this type of problem usually requires adjusting the underlying business model.

Growth-Driven Cash Flow Pressure

Some companies experience growth-driven cash flow pressure. Rapid expansion can require significant upfront investment before revenue increases. Purchasing inventory, hiring staff, or launching marketing campaigns all require capital. Without careful planning, even a growing business can experience cash shortages during periods of expansion.

Signs Your Business Has a Cash Flow Problem

Many businesses overlook early warning signs until the situation becomes urgent. Recognizing these signals can help prevent larger financial challenges and give business owners time to take corrective action before the problem escalates.

Common indicators of cash flow problems include:

- Difficulty paying suppliers on time

- Increasing reliance on credit or short-term borrowing to cover routine expenses

- Delaying payroll or other operational payments

- Postponing investments in equipment, marketing, or hiring

- Reducing inventory purchases due to limited cash

- Constantly reacting to short-term financial pressures instead of planning ahead

These warning signs often appear gradually, which is why they are easy to overlook at first. Paying attention to them as they come up can help businesses address cash flow challenges before they begin to disrupt day-to-day operations.

A 30-Day Plan to Stabilize Cash Flow

When a business starts running into cash flow challenges, taking a structured approach can help bring finances back under control. Instead of reacting to problems as they arise, it helps to focus on a short-term plan that prioritizes protecting available cash, bringing in revenue faster, and managing outgoing expenses. The following four-week framework outlines practical steps businesses can take to assess their financial situation, improve liquidity, and begin rebuilding a more stable cash position.

Week 1: Identify Immediate Cash Risks

Start by reviewing all outstanding invoices and identifying which payments are overdue. At the same time, prioritize essential expenses such as payroll, rent, and supplier payments. During this stage, it is also important to pause any non-essential spending so that available cash can be directed toward critical obligations.

Week 2: Accelerate Cash Inflows

Once immediate risks are identified, focus on bringing cash into the business faster. Contact customers with overdue invoices and establish clear payment expectations. Some businesses may offer small discounts for early payment or require deposits for new projects to improve cash flow timing.

Week 3: Reduce Cash Outflows

The next step is to control spending. Negotiating payment terms with suppliers can help align expenses with incoming revenue. Businesses should also review recurring expenses to determine whether any subscriptions, services, or discretionary purchases can be reduced or postponed.

Week 4: Build a Short-Term Cash Buffer

In the final stage, businesses should begin strengthening their financial resilience. Updating cash flow forecasts can help identify upcoming financial risks. Exploring short-term financing options or establishing a minimum cash reserve can also provide stability while longer-term improvements take effect.

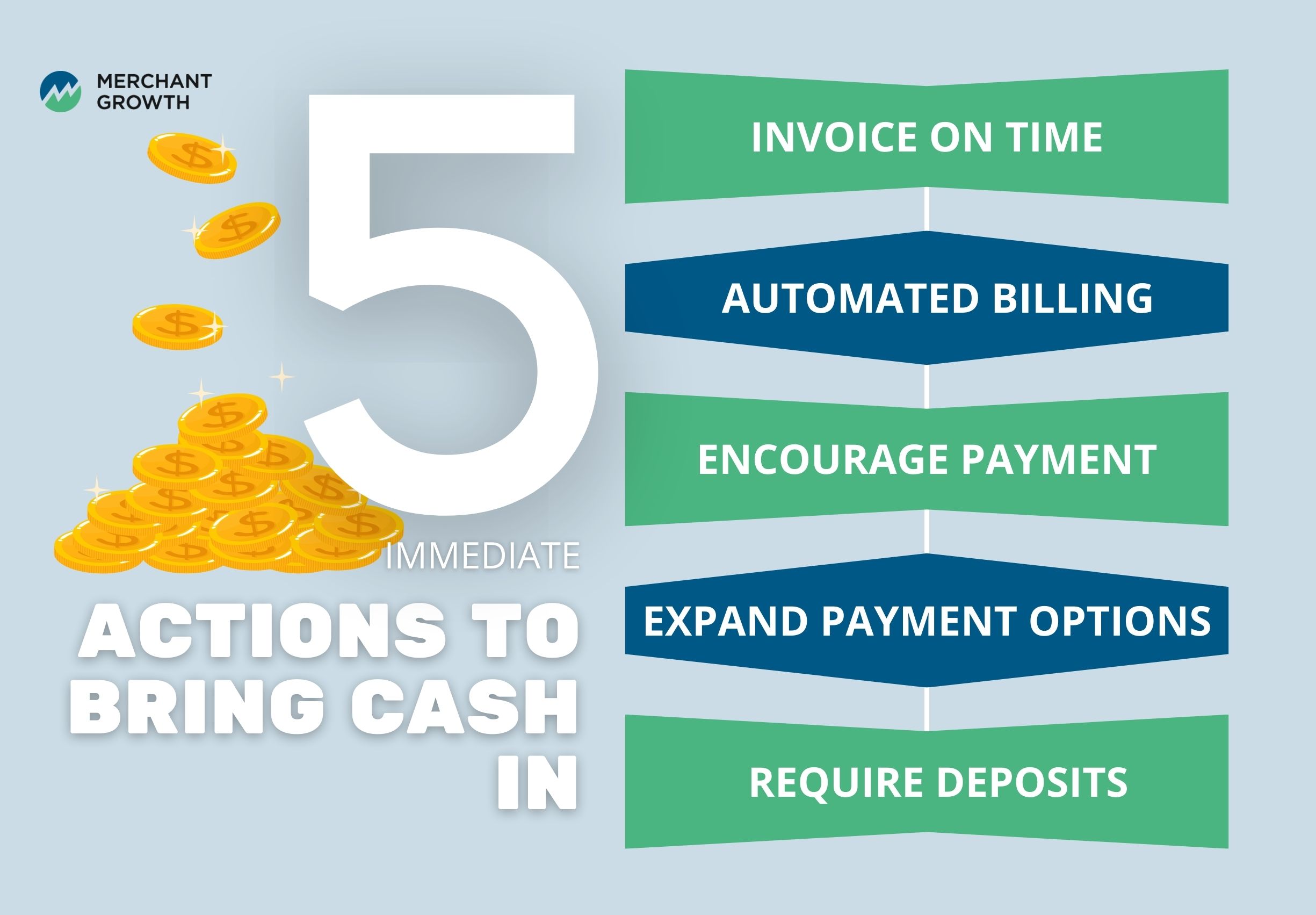

Immediate Actions to Improve Cash Coming In

Several operational adjustments can improve cash flow relatively quickly. Many of these changes focus on accelerating incoming payments and improving the way money moves through the business. By tightening invoicing processes and making it easier for customers to pay, businesses can often shorten payment cycles and reduce delays. Small adjustments in how payments are requested and collected can make a noticeable difference in how quickly cash comes in.

Practical steps that can help improve cash flow include:

- Send invoices immediately after work is completed. Prompt invoicing reduces delays and ensures customers receive payment requests as soon as possible.

- Use automated billing systems. Automation can streamline invoicing and help ensure invoices are sent consistently and on time.

- Encourage faster payments. Offering small discounts for early payment can motivate customers to settle invoices sooner.

- Expand payment options. Accepting credit cards or online payment platforms can make it easier for customers to pay promptly.

- Require deposits or milestone payments for larger projects. Collecting partial payments upfront helps cover initial costs before work is completed.

Strategies to Reduce Cash Outflows

While increasing revenue is important, managing expenses is equally critical for maintaining healthy cash flow. Businesses can improve financial stability by carefully controlling how and when money leaves the company. Reviewing spending patterns and adjusting payment terms can create more flexibility and help align outgoing expenses with incoming revenue. Even small changes in how costs are managed can make a meaningful difference in preserving available cash.

Ways to reduce cash outflows include:

- Negotiate longer payment terms with suppliers. Extended payment terms can help align expenses more closely with incoming revenue.

- Review and reduce non-essential spending. Evaluating discretionary expenses may reveal opportunities to cut costs without affecting core operations.

- Manage inventory levels carefully. Excess inventory ties up valuable working capital that could otherwise support daily operations.

- Delay non-critical purchases or investments. Postponing equipment upgrades or large purchases can help preserve cash during tighter periods.

Manage Your Cash Flow More Effectively

Managing cash flow effectively requires consistent attention rather than a one-time fix. Businesses that regularly monitor their finances are better able to spot potential issues early and take action before they become larger problems. Having a clear view of how money is moving in and out of the business allows owners to make more informed decisions about spending, investments, and future growth.

One of the most useful tools for maintaining control over cash flow is a forecast. By estimating future cash inflows and outflows, businesses can anticipate potential shortfalls and plan for upcoming expenses. Regularly reviewing financial reports can also reveal patterns in revenue and spending, helping business owners identify trends that may affect liquidity over time.

Preparation is another important part of strong cash flow management. Building a cash reserve can provide a financial cushion during slower periods or when unexpected expenses arise. Even a modest buffer can help businesses navigate temporary challenges without disrupting day-to-day operations. Modern accounting software and financial tools can further support this process by providing real-time insights that make it easier to track financial performance and plan ahead.

When to Consider Financing to Solve Cash Flow Problems

Even when businesses take the right steps to improve their cash flow, those changes don’t always produce results immediately. Adjusting payment terms, improving collections, or reducing expenses can take time to fully affect the flow of money through the business. In the meantime, companies still need to cover everyday costs such as payroll, supplier payments, and inventory purchases.

This is where access to additional working capital can play an important role. Financing can help businesses bridge temporary gaps in cash flow while they work on strengthening their financial processes. It may be used to cover short-term operating expenses, purchase inventory ahead of demand, or manage fluctuations in seasonal revenue.

When used thoughtfully, financing gives businesses the flexibility to keep operations running smoothly while longer-term improvements take effect. Instead of constantly reacting to short-term cash shortages, owners can focus on improving their processes, serving customers, and continuing to grow the business.

Preventing Future Cash Flow Problems

Solving cash flow problems is only part of the process. Preventing them from recurring requires consistent financial planning and ongoing monitoring. Businesses that regularly review their financial position are better able to anticipate potential challenges and make adjustments before they become serious disruptions.

Maintain a Reliable Cash Flow Forecast

Maintaining an accurate cash flow forecast allows businesses to anticipate potential shortfalls before they occur. By projecting future inflows and outflows, owners can identify periods where cash may become tight and plan accordingly. Regularly updating these forecasts also helps businesses adjust spending and investment decisions as financial conditions change.

Review Payment Terms and Expenses Regularly

Payment terms and spending patterns can have a significant impact on cash flow stability. Reviewing customer payment policies and tightening credit terms when necessary can help reduce delayed payments. At the same time, regularly monitoring expenses ensures that costs remain aligned with revenue and prevents unnecessary spending from eroding available cash.

Build a Cash Reserve

Building a financial buffer is another important step in preventing future cash flow issues. Maintaining a reserve of available cash allows businesses to absorb unexpected expenses or temporary revenue slowdowns. Even a modest reserve can provide stability and give business owners the flexibility to manage challenges without disrupting operations.

Turning Cash Flow Challenges Into Opportunities for Growth

Cash flow problems can feel overwhelming, but they are also a common part of running a business. Many companies experience periods of financial pressure as they grow, adapt to market conditions, or adjust their operations.

Businesses that take a proactive approach to managing cash flow often emerge stronger. By improving invoicing processes, controlling expenses, and forecasting future financial needs, business owners can build a more resilient financial foundation.

Merchant Growth supports Canadian small businesses by providing flexible financing solutions designed to help stabilize cash flow and support ongoing growth. Whether a business needs working capital to manage short-term expenses or funding to pursue new opportunities, access to the right financial tools can make a meaningful difference.