Finding out your loan application was denied can feel like a punch to the gut. You spent time preparing documents, outlining your plans, and explaining your business, only to hear “no.” It’s frustrating, and for many business owners, it can feel personal. But in reality, a loan denial is rarely about you as an entrepreneur. It’s about how a lender assesses risk, and whether your business fits within their specific lending criteria.

The truth is, many healthy businesses get declined for financing, especially by traditional banks. A loan application denied does not automatically mean your business is struggling or unviable. It often means there’s a mismatch between your business profile and that lender’s requirements. Understanding why business loan applications get denied, and what you can do next, puts you back in control.

This guide walks through the most common reasons for business loan rejection, what happens after a denial, how to strengthen your next application, and what alternatives exist when banks say no.

What Does “Loan Application Denied” Actually Mean?

When a lender denies your application for a business loan, it means their underwriting team determined the level of risk was too high based on their internal standards. Every lender has a different risk model, and those models evaluate several key factors before approving funding.

Typically, lenders look at:

- Your ability to repay the loan

- Your personal and business credit profile

- Your current cash flow

- Your existing debt obligations

- The stability of your industry

- The completeness and clarity of your documentation

A denial does not necessarily mean your business is failing. It may simply mean you don’t meet that lender’s current business loan requirements. In many cases, the same business declined by one lender may be approved by another with a different risk appetite or evaluation process.

The Top Reasons Business Loan Applications Get Denied

When a loan application is denied, it’s rarely for just one vague reason. Lenders rely on structured underwriting criteria to assess risk, and most rejections trace back to a handful of common factors. The challenge is that lenders don’t always provide detailed explanations, which can leave business owners guessing about what went wrong.

Understanding the most common reasons for business loan rejection can help you identify where your application may have fallen short, and more importantly, what you can improve before applying again. While every lender’s standards differ, the underlying themes are surprisingly consistent across banks and financial institutions.

Let’s break down the most common causes.

Weak or Inconsistent Cash Flow

Cash flow is one of the most important factors in the business loan application process. Lenders want to see predictable income that comfortably covers operating expenses and proposed loan payments. Even if your sales are strong on paper, irregular inflows, seasonal dips, or tight margins can raise concerns about repayment reliability.

This is why 41% of loan denials are tied to weak cash flow. Revenue tells lenders about growth potential, but cash flow tells them whether you can repay the loan on time, every time. In lending decisions, repayment capacity carries more weight than sales volume. A business generating steady, reliable cash flow will almost always appear lower risk than one with higher but inconsistent revenue.

Poor Personal or Business Credit

Your credit score still plays an important role in business loan applications. Many lenders review both your personal credit history and your business credit profile when assessing risk. Late payments, high utilization, or previous defaults can signal elevated risk.

Business owners often ask, “Can I get a business loan with bad credit?” The answer depends heavily on the lender. Traditional banks tend to maintain stricter credit thresholds, while alternative lenders may consider credit alongside cash flow performance and overall business strength. A lower credit score doesn’t automatically mean financing is impossible, but it can limit your options or affect pricing.

High Debt Load

If your business already carries significant debt, lenders may hesitate to approve additional financing. Debt-to-income ratios and overall leverage are closely examined to determine whether the business can reasonably take on more obligations.

Even profitable companies can face rejection if their existing debt payments consume too much of their monthly cash flow. From a lender’s perspective, adding more debt increases repayment risk, especially if margins are already tight. Demonstrating that your business has room to absorb new payments is essential in the approval process.

Lack of Collateral

Traditional lenders frequently require collateral to secure a loan. This could include equipment, property, inventory, or other tangible assets. If your business lacks sufficient assets to pledge, approval can become more difficult.

Statistics Canada reports that 32% of loan denials are linked to insufficient collateral. This can be particularly challenging for service-based businesses or newer companies that haven’t accumulated substantial physical assets. In these cases, the structure of the financing and the type of lender can significantly affect approval likelihood.

Incomplete or Weak Documentation

Strong documentation signals professionalism and financial control. Missing financial statements, inconsistent bookkeeping, unclear projections, or vague business plans can all weaken your application.

Even when the numbers are solid, poor presentation can create doubt. Lenders want to see accurate, organized, and transparent reporting. Clean documentation not only speeds up the review process but also builds confidence in your ability to manage capital responsibly.

Limited Time in Business

Startups and early-stage companies are statistically considered higher risk. If your business has been operating for less than two years, approval may be more challenging, particularly with traditional banks that prioritize established operating history.

This doesn’t mean young businesses can’t secure financing. It simply means lenders may evaluate them differently, often placing greater emphasis on projections, personal credit, and management experience.

Understanding these factors helps turn rejection from a mystery into a roadmap. Once you know what lenders are evaluating, you can begin strengthening those areas intentionally.

In the next section, we’ll look at what to do immediately after a loan denial, and how to turn that setback into a smarter, stronger application moving forward.

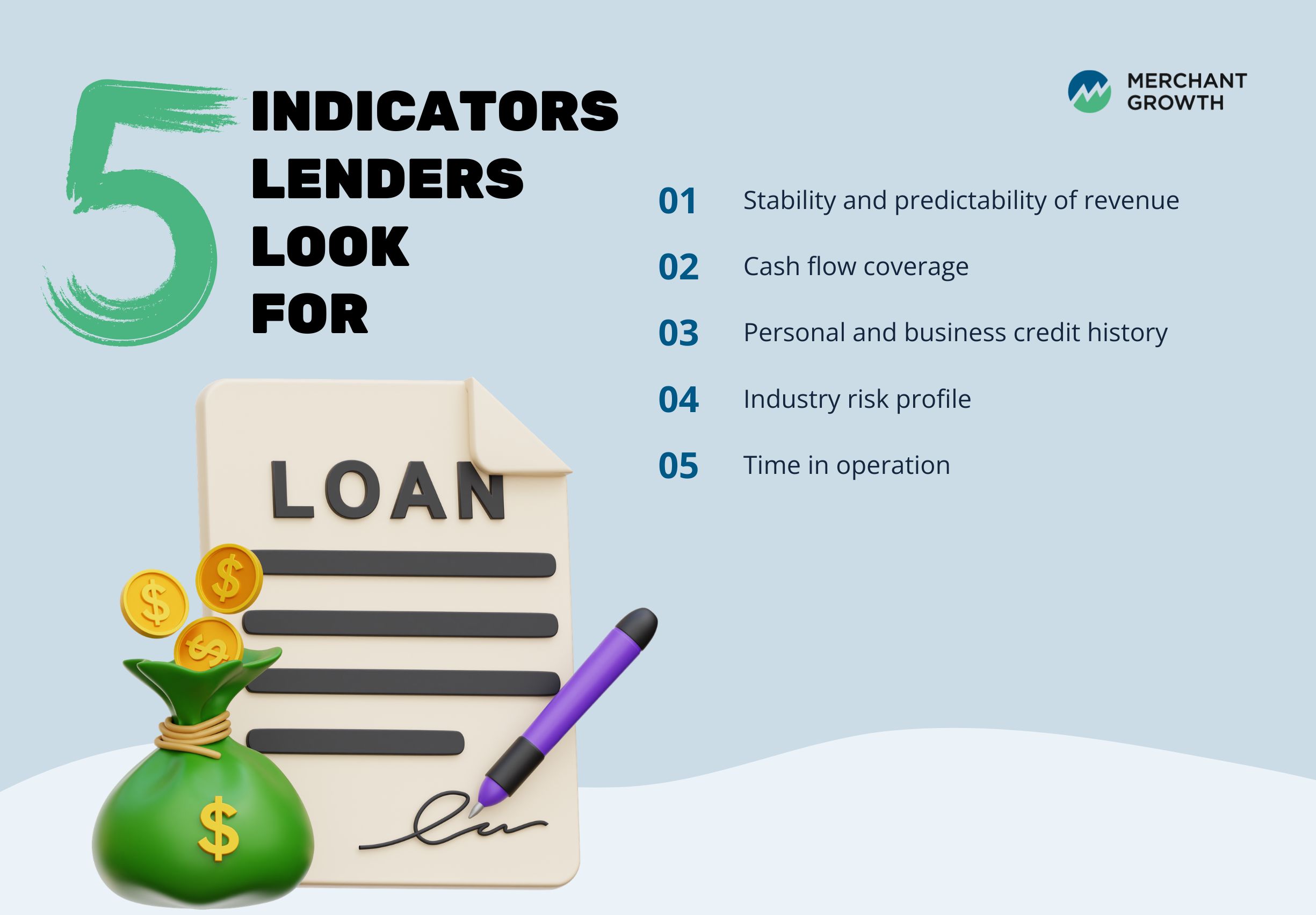

How Likely Are You to Be Approved for a Business Loan?

One of the most common questions business owners ask after a loan application is denied, or before they even apply, is: What are my actual chances of getting approved? The honest answer is that approval isn’t based on a single number or a quick checklist. Lenders look at a combination of factors to determine how risky it would be to extend financing to your business.

Some factors carry more weight than others depending on the lender’s underwriting model, but most financial institutions evaluate a core set of indicators when reviewing business loan applications.

Typically, lenders look at:

- Stability and predictability of revenue

- Cash flow coverage relative to proposed loan payments

- Personal and business credit history

- Industry risk profile

- Time in operation

Each of these factors helps lenders answer one central question: Can this business repay the loan consistently and on time? Strong revenue growth can help, but predictable cash flow and responsible credit behaviour often carry more influence in the final decision.

Traditional banks generally apply stricter, standardized approval criteria, particularly around credit scores, collateral, and operating history. Alternative lenders may assess risk more dynamically, weighing real-time revenue performance and broader business trends alongside credit metrics. That’s why two lenders reviewing the exact same application can reach completely different conclusions.

If you’re wondering how to get a small business loan, the first step is understanding what lenders are really evaluating, not just what they advertise on their websites. When you know which levers influence approval odds, you can take practical steps to strengthen your position before submitting your next application.

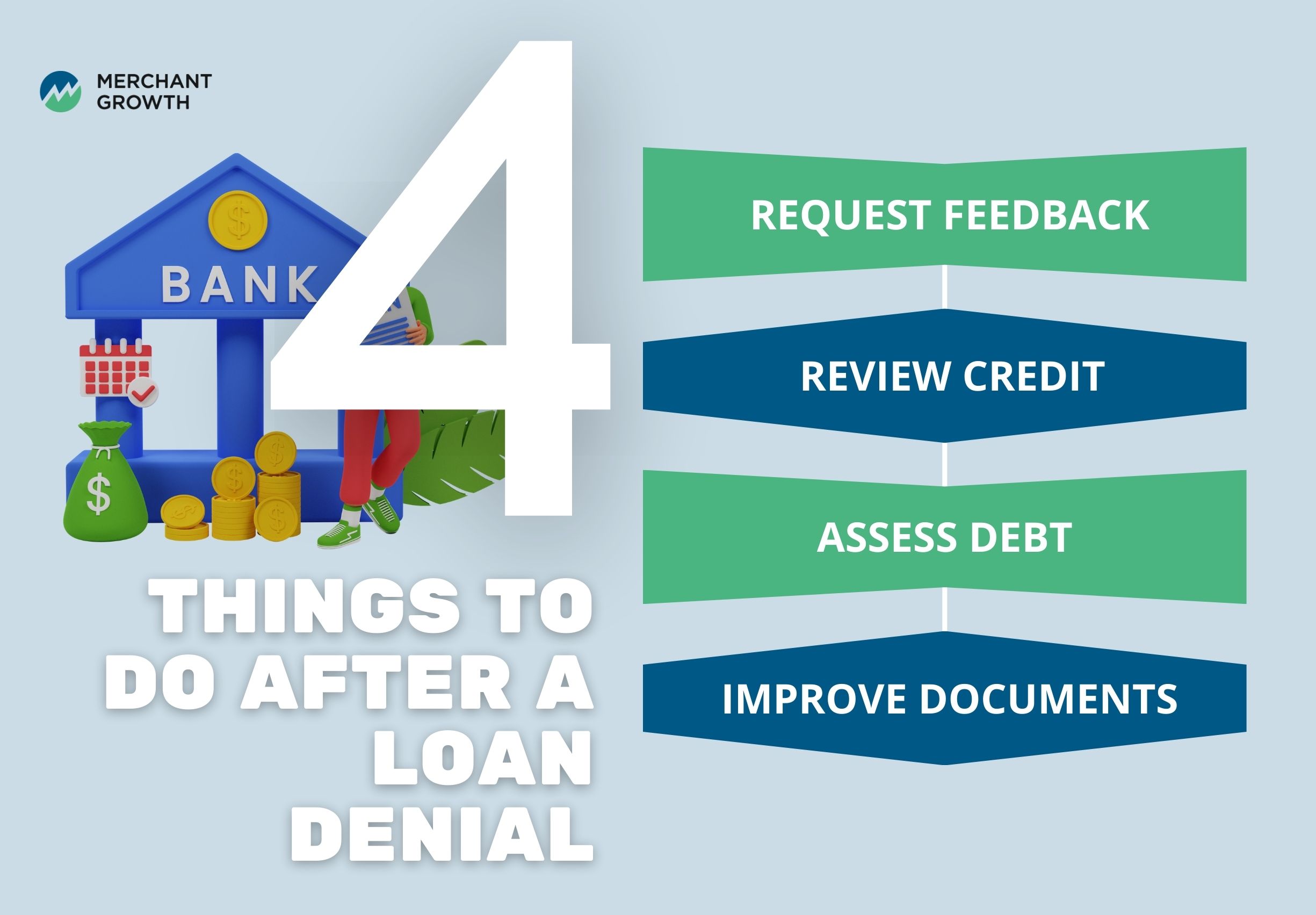

What to Do Immediately After a Loan Denial

A loan rejection can feel discouraging, but it’s important to pause before reacting emotionally. A denial is not a final verdict on your business, it’s feedback. When approached strategically, it can actually strengthen your next application and improve your long-term financing readiness. The key is to treat the experience as diagnostic rather than definitive.

Instead of asking, “Why did this happen to me?” the better question is, “What can I learn from this?” Here’s how to respond productively.

Request Specific Feedback

Your first step should be to ask the lender for detailed feedback about why the application was declined. While not all institutions provide in-depth explanations, many will outline the primary reason for the decision. This could include credit score thresholds, insufficient cash flow coverage, high leverage ratios, or documentation gaps.

Understanding the exact reason matters because it determines your next move. For example, if the issue was cash flow coverage, you may need to focus on improving margins or reducing expenses. If it was credit-related, you’ll know to prioritize score improvement before reapplying. Clear feedback transforms a vague rejection into a concrete action plan.

Review Your Credit Profile

Your personal and business credit reports play a larger role in business loan applications than many owners realize. After a denial, request copies of your credit reports and review them carefully for inaccuracies. Even minor reporting errors, such as outdated balances or misreported late payments, can negatively impact your approval chances.

Beyond correcting errors, it’s important to understand where your score sits relative to typical lending benchmarks. Traditional banks often require stronger credit profiles, while alternative lenders may evaluate credit alongside real-time performance metrics. Knowing your position helps you target the right type of lender and avoid unnecessary rejections in the future.

Assess Cash Flow and Debt Structure

Cash flow is one of the most common reasons business loan applications get denied. Take a detailed look at your monthly revenue trends, recurring expenses, and existing debt obligations. Ask yourself whether your business could comfortably absorb additional loan payments without straining operations.

This is also a good time to evaluate whether discretionary expenses can be reduced or whether supplier payment terms can be renegotiated. Even modest improvements in monthly free cash flow can significantly strengthen financial ratios. Lenders want to see stability and repayment capacity; small operational adjustments can make a meaningful difference.

Strengthen Financial Documentation

Clean, organized documentation builds lender confidence. If your application included incomplete financial statements, unclear projections, or inconsistent bookkeeping, now is the time to address those gaps. Update your profit and loss statements, balance sheets, and cash flow reports so they accurately reflect your current position.

It’s also helpful to prepare realistic projections that clearly explain how the loan will support growth and generate returns. Lenders want to see thoughtful planning, not just optimistic forecasts. Transparency, consistency, and professionalism in your documentation demonstrate that you are managing your business with discipline and foresight.

Taking these steps doesn’t just prepare you for your next application; it strengthens your business overall.

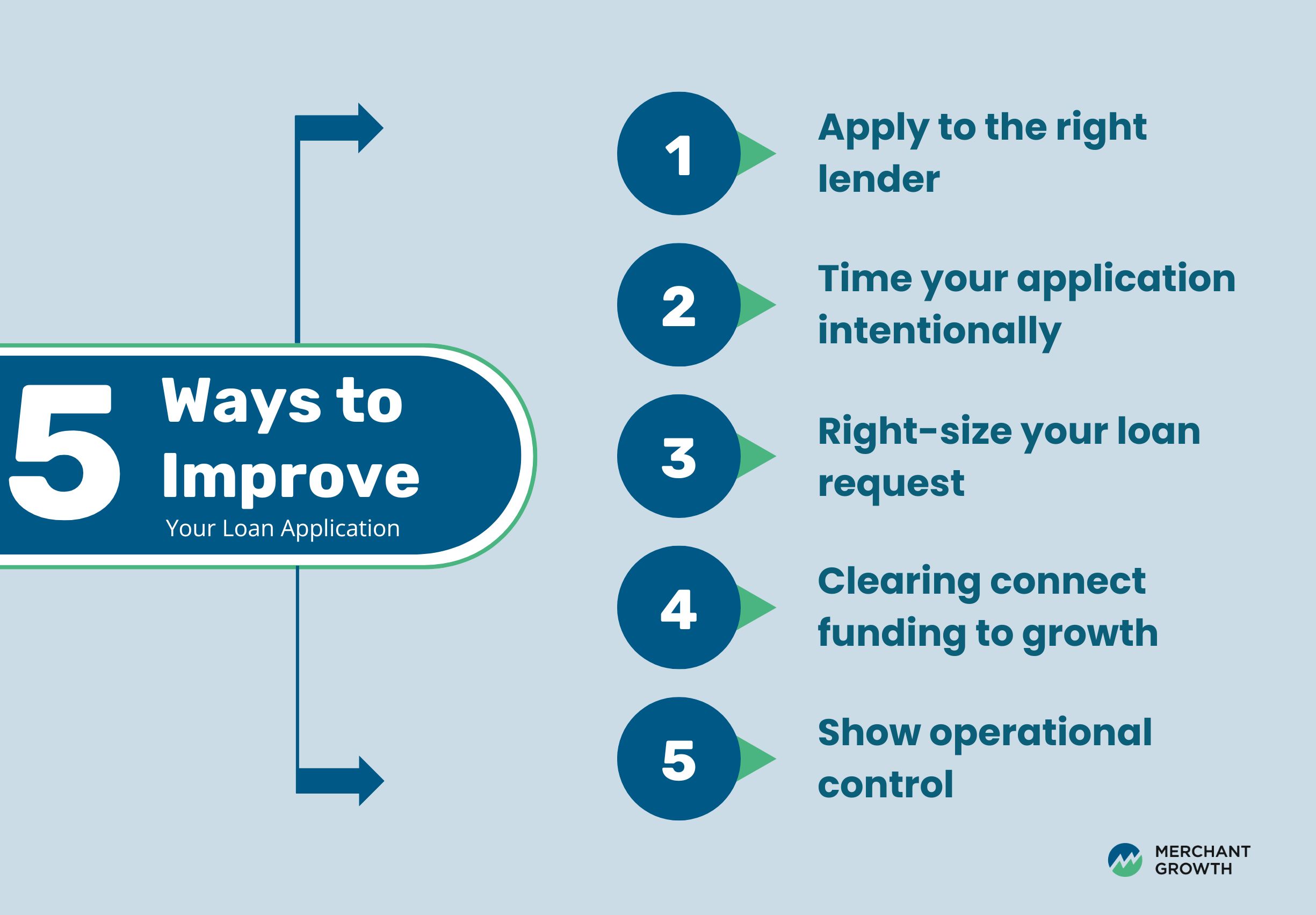

How to Strengthen Your Next Loan Application Strategically

If you’re preparing to apply again, the goal isn’t just to correct past issues; it’s to position your business more effectively. Financing decisions are about risk alignment. The better you understand how lenders evaluate applications, the more strategically you can present your business.

Apply to the Right Type of Lender

Not all lenders assess risk the same way. Traditional banks often emphasize collateral, long operating history, and strong credit benchmarks. Alternative lenders may focus more on current cash flow performance and revenue stability. Understanding this difference is essential when navigating the business loan application process. Matching your business profile to the right lender can dramatically improve approval odds.

Time Your Application Intentionally

Timing plays a larger role than many business owners realize. If your revenue has recently dipped due to seasonality or temporary disruption, waiting until performance stabilizes can improve how your numbers are evaluated. Lenders typically review recent financial activity closely, so applying during a strong revenue cycle can strengthen your case.

Right-Size Your Loan Request

One common reason business loan applications are declined is that the requested amount exceeds what the business can realistically support. When considering how to get a small business loan, it’s important to align your request with your revenue and repayment capacity. A realistic, well-supported funding request signals financial discipline and reduces perceived risk.

Clearly Connect Funding to Growth

Lenders are more comfortable approving loans that are tied to measurable business outcomes. Whether you’re investing in inventory, hiring, marketing, or equipment, clearly explain how the funds will generate return. Demonstrating that you have a plan, not just a need, strengthens your application significantly.

Show Operational Control

Strong financial documentation is important, but so is your ability to explain your numbers. When you can confidently discuss revenue trends, margins, and projections, you demonstrate control and oversight. That credibility can make a meaningful difference in how lenders perceive your business.

When Banks Say No: Exploring Alternative Financing Options

If traditional lenders decline your application, that doesn’t mean financing is off the table. Many Canadian small businesses secure funding through alternative channels every year, especially when banks apply stricter requirements around credit, collateral, or operating history.

The financing landscape today is broader than it was even a decade ago. In addition to traditional banks, business owners can explore a range of funding sources that may better match their stage of growth, revenue structure, or industry type. Some common alternatives include:

- Non-bank lenders

- Online financing platforms

- Revenue-based financing

- Government programs

- Smaller structured loans

Each option comes with its own structure, eligibility criteria, and repayment model. The key is understanding how these lenders evaluate risk and whether their approach aligns with your business’s strengths.

Unlike many traditional banks, alternative lenders often assess businesses more holistically. Instead of focusing exclusively on credit score or physical collateral, they may consider a broader range of performance indicators, such as:

- Real-time revenue performance

- Cash flow trends

- Overall business stability

Technology-driven underwriting has changed how some lenders evaluate applications. By analyzing up-to-date financial data and revenue patterns, they can form a more current picture of business health. This doesn’t mean standards are lower, it simply means the evaluation process may be different.

For many businesses, especially those with steady revenue but limited collateral or shorter operating history, this broader assessment model can open doors that traditional lending frameworks may not.

Why Rejection Isn’t the End of the Road

Traditional banks operate under strict regulatory frameworks and conservative underwriting models. Their criteria are often rigid, and many growing businesses simply don’t fit inside those parameters yet.

The reality is that risk models vary. Some lenders prioritize collateral. Others focus on historical credit. Still others, including Merchant Growth, focus on real business performance and forward-looking potential.

Many businesses that are declined by banks still qualify for structured growth financing. The key is finding a lender whose evaluation process matches your business stage and trajectory. Financing should support growth, not penalize ambition.

Financing Readiness Is Ongoing, Not Just After a Rejection

Loan approval isn’t a one-time event. Financial health is something you build continuously. Maintaining organized books, steady cash flow, manageable debt levels, and clear growth plans improves optionality over time.

When your financial fundamentals are strong, you have more choices. And having choices is one of the most powerful positions a business owner can be in.

From Rejection to Resilience

A loan application denied can feel discouraging, but it can also be a turning point. Many successful businesses have faced initial rejection before finding the right financing partner.

The key isn’t avoiding rejection entirely. It’s understanding why it happened, strengthening your foundation, and exploring options that fit your business reality.

If your loan application was denied, it doesn’t mean your business isn’t viable, it means you need the right financing partner. Merchant Growth works with Canadian small businesses to provide flexible funding solutions designed to support real growth, even when traditional lenders aren’t an option.