For many Canadian small business owners, the biggest tax bill they ever face does not come from day-to-day operations; it comes from growth. The moment you sell a commercial property, cash out a profitable investment, or begin planning the eventual sale of your business, conversations around capital gains suddenly become impossible to ignore. What once felt like a distant tax concept quickly turns into a major financial decision that can affect how much of your hard-earned profit you actually keep.

The challenge is that many entrepreneurs do not think about capital gains until they are already facing them. After years spent building a business, growing assets, and reinvesting into expansion, it can be surprising to learn how much taxes may impact the final outcome of a sale. That is why understanding capital gains is not just about tax compliance; it is about protecting the value you worked years to create.

What Is a Capital Gain?

A capital gain is the profit earned from selling an asset that has increased in value. For small business owners, these assets can include

- investments

- commercial real estate

- equipment

- business shares

- even an entire company.

If the selling price exceeds the original purchase price, the difference is generally considered a capital gain.

For example, imagine a business owner purchases a warehouse for $500,000 and later sells it for $750,000 after several years of appreciation. The increase in value creates a capital gain. The same concept applies if an entrepreneur invests excess business cash into stocks or ETFs and later sells those investments for a profit.

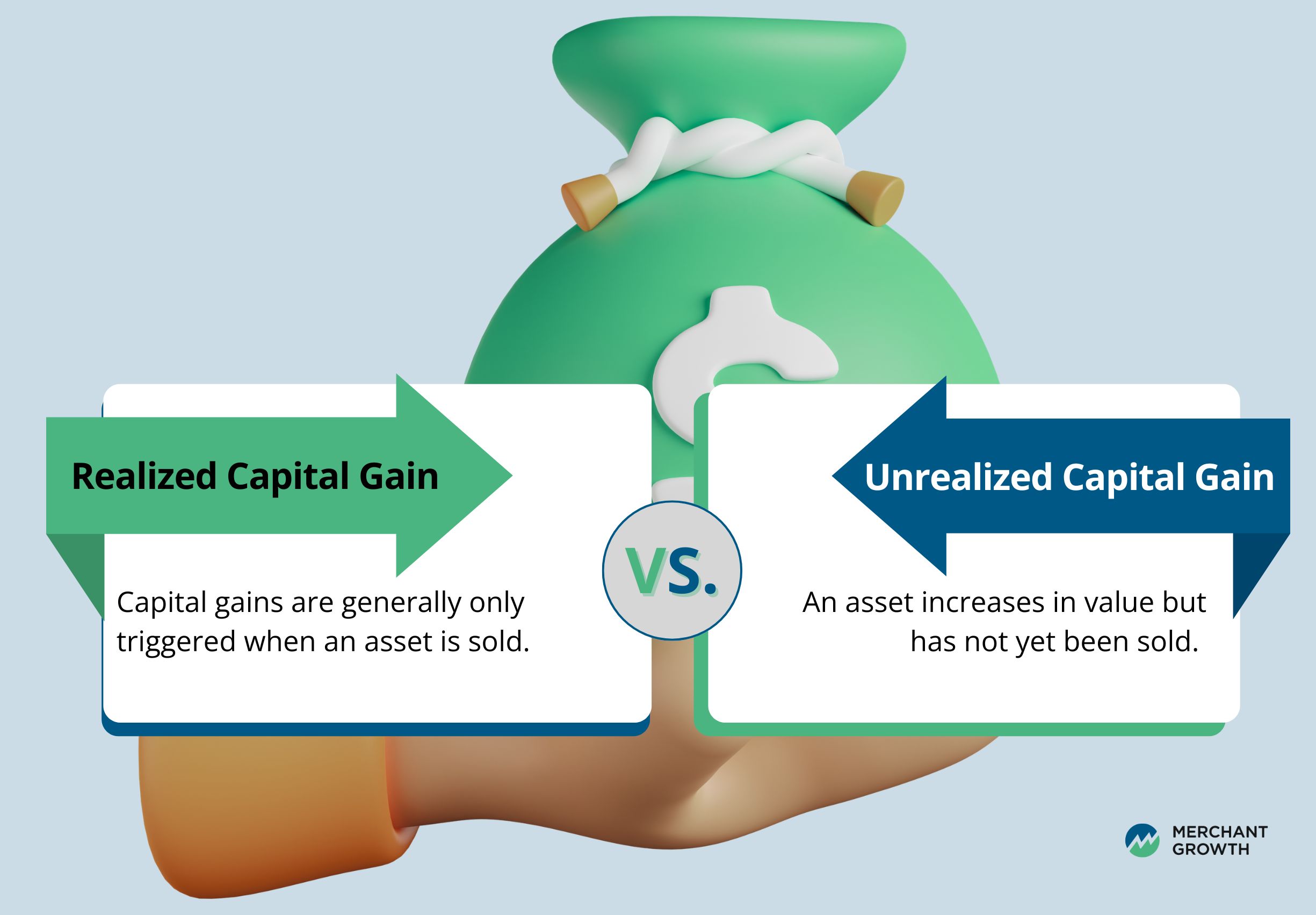

Realized vs Unrealized Capital Gains

One of the most important things for business owners to understand is that capital gains are generally only triggered when an asset is sold. This is known as a realized capital gain. While an investment, commercial property, or business asset may increase in value over time, the gain itself is not typically taxable until the sale actually happens.

An unrealized capital gain, on the other hand, happens when an asset increases in value but has not yet been sold. This distinction is important because it gives entrepreneurs more flexibility around timing, financial planning, and long-term wealth management.

Capital Gains vs Business Income

Many business owners confuse capital gains with business income, but the two are taxed very differently in Canada. How the CRA classifies your earnings can have a major impact on how much tax you ultimately pay.

Capital gains are typically earned from selling long-term assets like investments, commercial property, or business shares for a profit. In Canada, only 50% of a capital gain is considered taxable income. For example, if you earn a $100,000 capital gain, generally only $50,000 is added to your taxable income.

Business income, on the other hand, is generated through ongoing commercial activity, such as selling products or services or actively trading investments. Unlike capital gains, 100% of business income is taxable.

How business income is taxed also depends on your business structure. Sole proprietors report income on their personal tax return, while incorporated businesses pay corporate tax rates on active business income. Many Canadian-controlled private corporations (CCPCs) qualify for lower small business tax rates on eligible income, although provincial taxes also apply.

The distinction becomes especially important with investment activity. A business owner making occasional long-term investments may generate capital gains, while someone frequently trading stocks or cryptocurrency for short-term profit could have earnings classified as fully taxable business income instead.

What Assets Can Create Capital Gains for Business Owners?

Capital gains are not limited to stock market investing. For many Canadian entrepreneurs, capital gains are triggered during major business or financial milestones, such as selling property, restructuring ownership, or investing retained earnings outside the business.

Some capital gains are directly connected to business operations, while others come from personal or corporate investments used to build long-term wealth. Understanding the difference can help business owners plan more effectively and avoid unexpected tax obligations later on.

Business Assets and Commercial Property

Commercial real estate is one of the most common sources of capital gains for business owners. If a company-owned office, warehouse, retail space, or investment property increases in value and is later sold, the profit may create a capital gain.

Many entrepreneurs purchase property as part of long-term growth planning, especially when expanding operations or building additional income streams. Over time, rising property values can create significant gains that affect taxes owed during the year of sale.

Selling Shares in a Business

For many entrepreneurs, their business itself is their largest capital asset. If a business owner eventually sells shares in their company, the sale may trigger capital gains taxes depending on how the transaction is structured.

This becomes especially important during succession planning, acquisitions, or retirement planning. In some cases, qualifying business owners may also be eligible for the Lifetime Capital Gains Exemption (LCGE), which can help reduce taxes on the sale of qualifying small business shares.

Stocks, ETFs, and Corporate Investments

Some business owners invest retained earnings into stocks, ETFs, or other long-term investments to grow excess cash outside daily operations. These investments can generate capital gains when sold for more than their adjusted purchase price.

However, gains are generally only triggered once the investments are sold and profits become realized. This is why many entrepreneurs carefully time investment sales as part of broader tax planning strategies.

Rental and Investment Properties

Many entrepreneurs invest in rental properties outside their primary business as a way to diversify income and build long-term wealth. While these properties can appreciate significantly over time, selling them may create substantial capital gains taxes.

Unlike a primary residence, rental and investment properties are generally taxable when sold at a profit. This often catches business owners off guard, especially if the property has appreciated over many years.

Cryptocurrency and Alternative Investments

Cryptocurrency has become increasingly popular among entrepreneurs and investors, but many business owners still misunderstand how crypto profits are taxed. Selling cryptocurrency for profit can create capital gains, even if the transactions occur entirely online.

The CRA may also classify frequent crypto trading as business income instead of capital gains if the activity resembles active trading. This distinction can significantly affect how profits are taxed.

How Capital Gains Tax Works in Canada

One of the biggest misconceptions about capital gains taxes is that the entire profit from a sale is taxed directly. In Canada, only 50% of a capital gain is currently considered taxable income. This taxable portion is known as a taxable capital gain and is added to the business owner’s total income for the year.

Why Capital Gains Are More Tax-Efficient Than Business Income

Capital gains are generally considered more tax-efficient than regular business income because only half of the gain is taxable. By comparison, 100% of active business income is subject to taxation.

This distinction can significantly affect long-term financial planning for business owners. Entrepreneurs often use investments, commercial real estate, or retained earnings strategies to build wealth over time, and capital gains treatment can help preserve more of those returns.

Why Timing Matters When Selling Assets

The timing of a sale can also have a major impact on taxes owed. Because taxable capital gains are added to annual income, selling multiple appreciating assets in the same year can increase taxable income substantially and potentially push a business owner into a higher tax bracket.

For incorporated businesses, the rules can become even more complex. Corporate investment income, passive income thresholds, shareholder structures, and the type of asset being sold can all affect how gains are taxed. In some cases, qualifying business owners may also be eligible for the Lifetime Capital Gains Exemption (LCGE), which can significantly reduce taxes on the sale of qualifying small business shares.

Because of these variables, many entrepreneurs work closely with accountants or tax advisors before selling major assets or restructuring ownership. Proactive planning often plays a major role in preserving long-term business wealth and reducing unexpected tax consequences.

How to Calculate Capital Gains

Calculating capital gains can feel intimidating at first, especially for entrepreneurs managing multiple investments or business assets. But once the process is broken into steps, it becomes much easier to understand. The key is maintaining organized records and understanding which numbers affect the final calculation.

Selling Price

The selling price refers to the total amount received when the asset is sold. This includes the proceeds earned from selling investments, real estate, or business shares. For larger business transactions, the selling price may include multiple components depending on how the deal is structured.

Accurately documenting the final sale amount is important because it serves as the starting point for calculating the capital gain. Without clear records, business owners may struggle to report gains properly during tax season.

Purchase Price

The purchase price is the original amount paid to acquire the asset. This figure establishes the baseline used to determine whether a profit was earned when the asset is eventually sold.

For long-term business owners, this can become more complicated over time. Assets may have been purchased years earlier, inherited, transferred between owners, or improved significantly since the original purchase date. Keeping accurate records from the beginning helps simplify future calculations.

Adjusted Cost Base (ACB)

Adjusted Cost Base, often referred to as ACB, is one of the most misunderstood parts of capital gains calculations. ACB represents the adjusted value of the asset after accounting for additional purchases, reinvestments, improvements, or certain eligible costs.

For example, if a business owner purchases additional shares of the same investment over time, the adjusted cost base changes. Similarly, major improvements to a property may affect the adjusted value used for tax calculations later. Understanding ACB is essential because inaccurate calculations can lead to overpaying or underreporting taxes.

Fees and Commissions

Certain expenses related to buying or selling an asset may reduce the taxable capital gain. Realtor commissions, legal fees, brokerage fees, and transaction costs can often be factored into the calculation.

For business owners selling commercial property or shares in a company, these expenses can become significant. Maintaining documentation for all transaction-related costs helps ensure gains are calculated accurately and efficiently.

The Capital Gains Formula

At its simplest level, the capital gains formula looks like this:

Selling Price – Adjusted Cost Base – Eligible Expenses = Capital Gain

For example, imagine an entrepreneur sells commercial property for $800,000. The adjusted cost base is $600,000, and eligible selling expenses total $25,000. In this scenario, the capital gain would be $175,000.

Once the gain is calculated, only a portion becomes taxable income under Canadian tax rules. That taxable amount is then added to the owner’s overall income for the year.

How Canadians Reduce Capital Gains Tax Legally

For business owners, reducing taxes legally is usually less about avoidance and more about strategic planning. Entrepreneurs who understand capital gains early often have more flexibility when managing investments, succession planning, and long-term wealth creation.

Proactive tax planning helps business owners preserve more of their returns while avoiding unnecessary surprises later. The goal is not to avoid taxes entirely, but to structure financial decisions in a way that improves long-term efficiency.

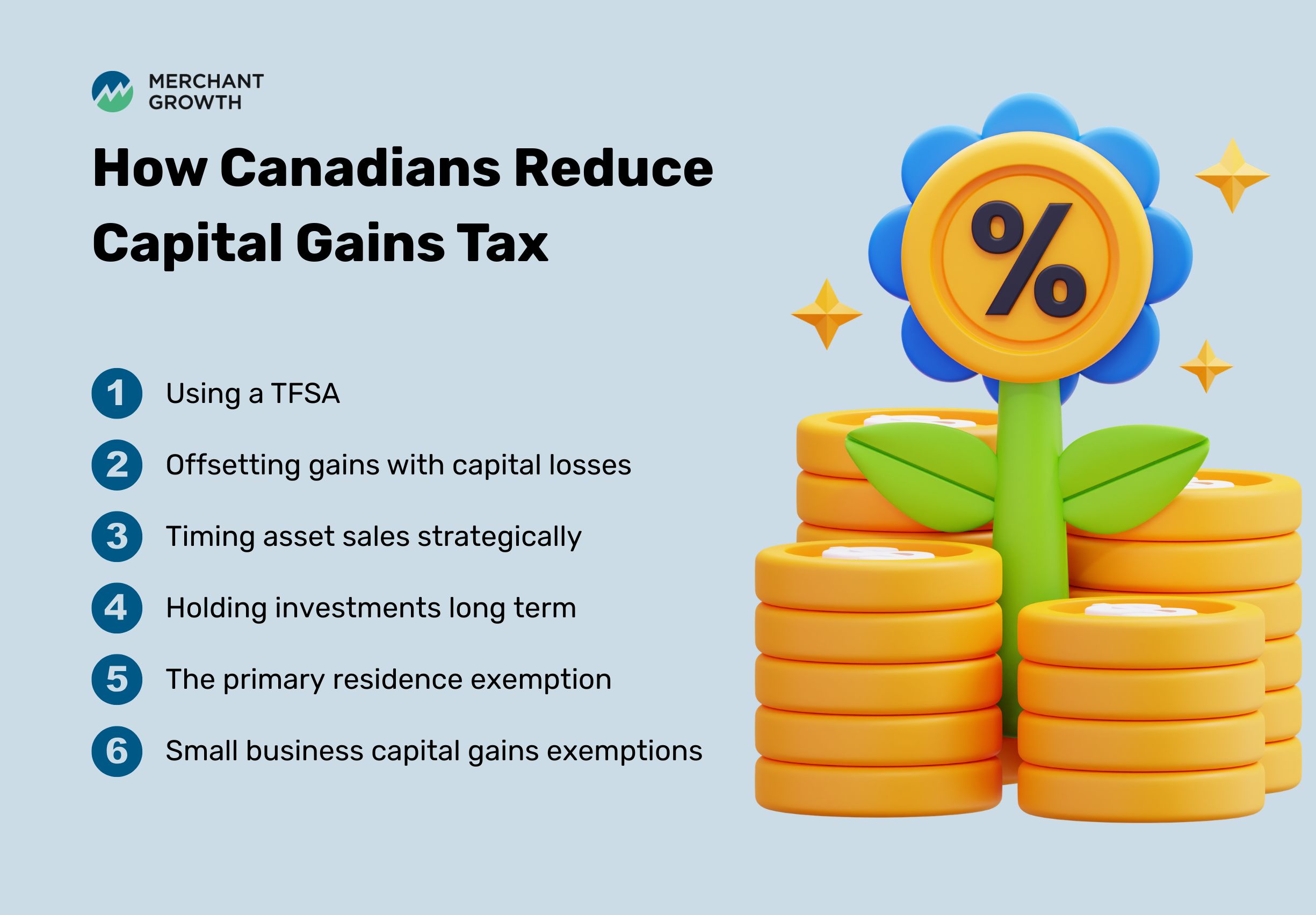

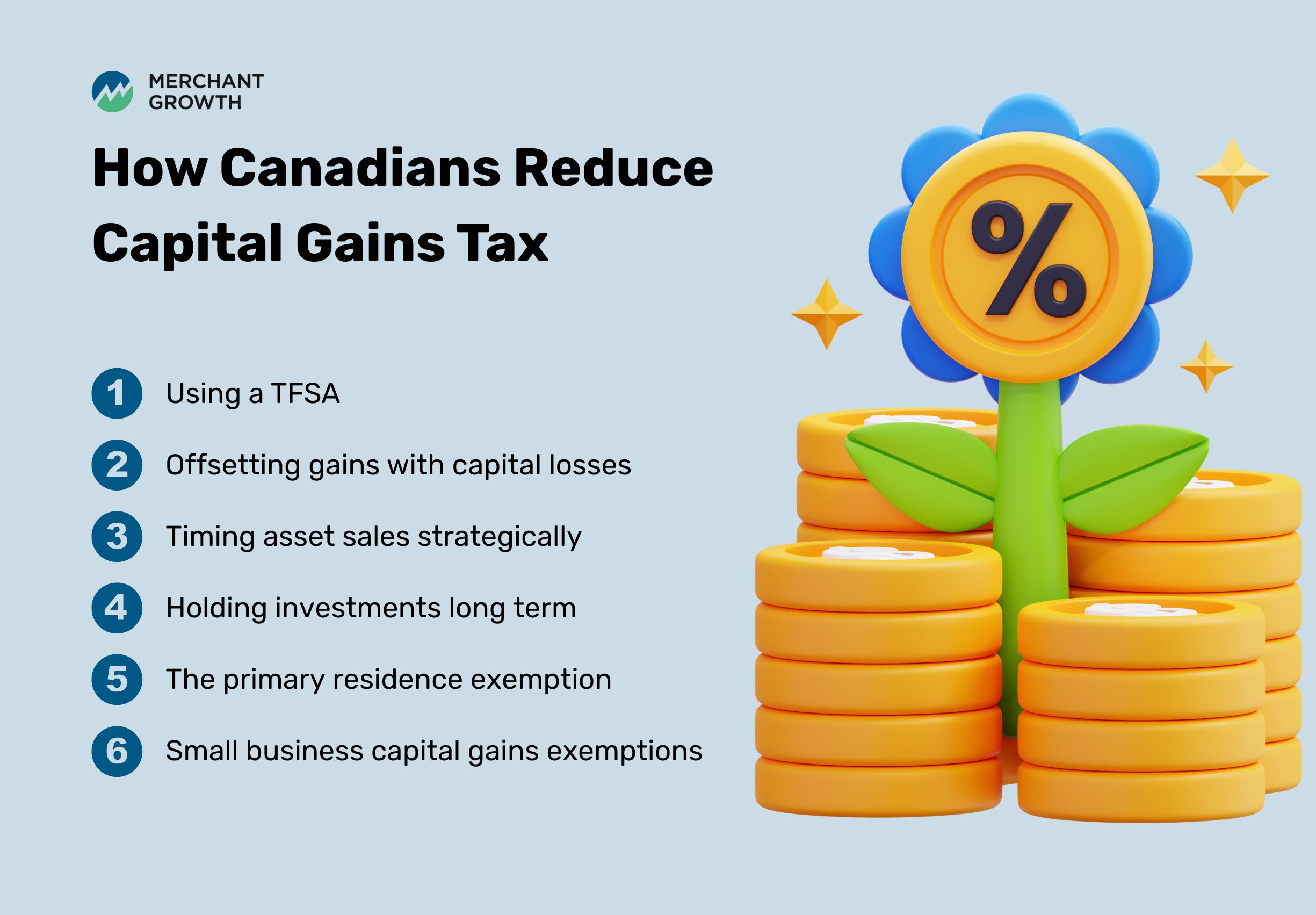

Using a TFSA

Tax-Free Savings Accounts (TFSAs) are one of the most effective tools available for growing investments without triggering capital gains taxes. Investments held inside a TFSA can generally grow tax-free, meaning gains earned within the account are not taxed when investments are sold.

For entrepreneurs investing outside their business, TFSAs can provide valuable flexibility. They allow business owners to build personal wealth more efficiently while reducing future tax exposure on investment growth.

Offsetting Gains with Capital Losses

Capital losses can help reduce taxes by offsetting taxable capital gains earned elsewhere. If an entrepreneur sells one investment at a profit and another at a loss, the loss may help reduce the taxable portion of the gain.

Some business owners intentionally review underperforming investments near year-end as part of tax planning strategies. This approach, often referred to as tax-loss harvesting, can help improve overall after-tax returns over time.

Timing Asset Sales Strategically

Timing plays a major role in how much tax a business owner ultimately pays. Selling multiple appreciating assets in the same year can create large spikes in taxable income, potentially increasing the total tax burden.

Many entrepreneurs strategically spread major sales across multiple years or plan transactions during lower-income periods. This type of proactive planning often creates more flexibility and better long-term financial outcomes.

Holding Investments Long Term

Long-term investing is often more tax-efficient than frequent buying and selling. Constant trading can create repeated taxable events that increase complexity and tax exposure over time.

For business owners focused on long-term growth, holding investments longer may help reduce unnecessary taxes while supporting more stable wealth accumulation. This approach also aligns with broader business planning and retirement goals.

The Primary Residence Exemption

In many cases, Canadians do not pay capital gains tax when selling their primary residence because of the principal residence exemption. However, this exemption does not automatically apply to rental properties, cottages, or investment real estate.

Business owners who own multiple properties should understand how these rules apply to different types of real estate. Misunderstanding the exemption can lead to unexpected tax obligations during future property sales.

Small Business Capital Gains Exemptions

The Lifetime Capital Gains Exemption (LCGE) can provide substantial tax savings for qualifying business owners. Eligible entrepreneurs may be able to shelter a significant portion of gains earned from selling qualifying small business corporation shares.

For many business owners, this exemption becomes especially important during succession planning or eventual business exits. Proper planning ahead of a sale can significantly improve the long-term financial outcome of selling a business.

Why Understanding Capital Gains Matters for Business Owners

Many entrepreneurs spend years focused on growth, operations, and revenue without thinking deeply about how taxes will affect their long-term wealth. But eventually, most business owners reach financial milestones where capital gains become highly relevant. Selling investments, transitioning ownership, or preparing for retirement can all create major taxable events.

Understanding capital gains allows business owners to make smarter decisions long before those moments happen. Instead of treating taxes as a last-minute issue, entrepreneurs can integrate tax efficiency into broader business and financial planning strategies.

There is also a mindset shift that happens when business owners fully understand how capital gains work. Taxes become less intimidating and more manageable. That confidence often leads to clearer decisions around investing, expansion, acquisitions, and long-term growth planning.

For Canadian small business owners, capital gains are not just a tax concept. They are closely connected to business value, financial growth, succession planning, and long-term wealth preservation. The sooner entrepreneurs understand how they work, the better positioned they are to protect the value they have spent years building.