- Add back non-cash expenses like depreciation.

- Subtract increases in non-cash revenues such as accrued revenue.

- Include net figures from investing and financing activities.

This gives you a complete view of your business’s actual cash movement. Regularly calculating

cash flow can help you identify bottlenecks or opportunities for improvement.”

}

}]

}

Cash flow is one of the most important indicators of a business’s financial health, yet it is also one of the most misunderstood. For many small business owners, cash flow becomes a concern only when a shortage appears. The reality is that healthy cash flow is not just about having enough money to cover today’s bills. It is about having the financial stability to operate confidently, plan ahead, and grow without unnecessary stress.

In simple terms, cash flow management is the process of tracking how money moves in and out of your business and making sure you always have enough available to meet your obligations. That includes paying suppliers, covering payroll, keeping up with tax remittances, and managing loan payments. A business with strong cash flow can act quickly on new opportunities, handle seasonal fluctuations, and avoid financial strain.

Research consistently shows how essential this is. According to M&F Bank, 82% of business failures can be linked to poor cash flow. Understanding how to manage it effectively can give your business the resilience it needs to thrive in any economic climate.

What Is Cash Flow (and Why It Matters)

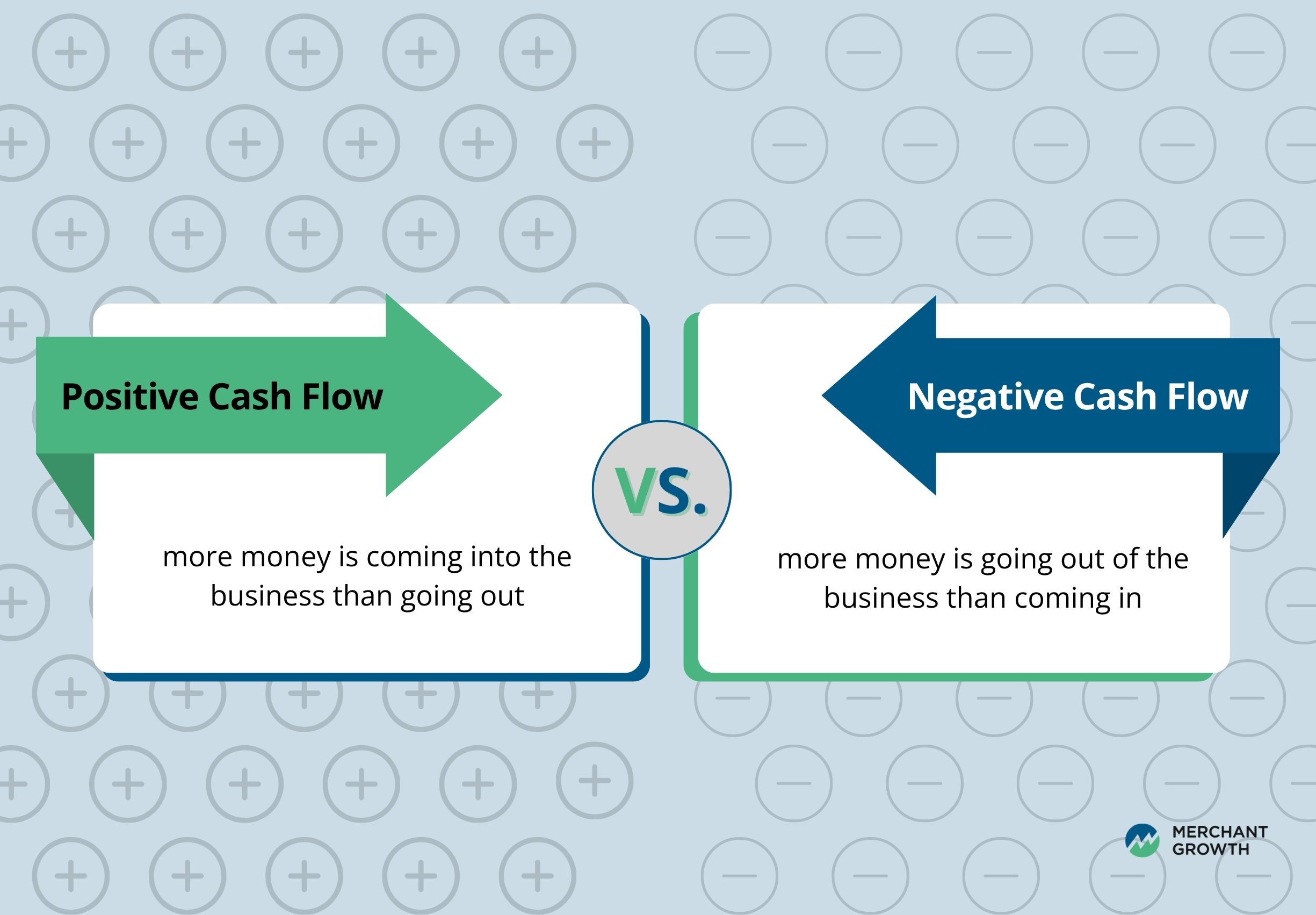

Cash flow is the movement of money into and out of your business over a specific period of time. In simple terms, cash flow equals the cash coming in from sales, collections, and other income minus the cash going out for expenses, payroll, inventory, and loan payments. It is the real-time financial heartbeat of your business, showing whether you have enough money on hand to operate today, tomorrow, and next month.

Positive cash flow occurs when more money flows in than flows out. Negative cash flow happens when expenses outpace income, which can quickly lead to missed payments, operational setbacks, and financial stress if it continues for too long.

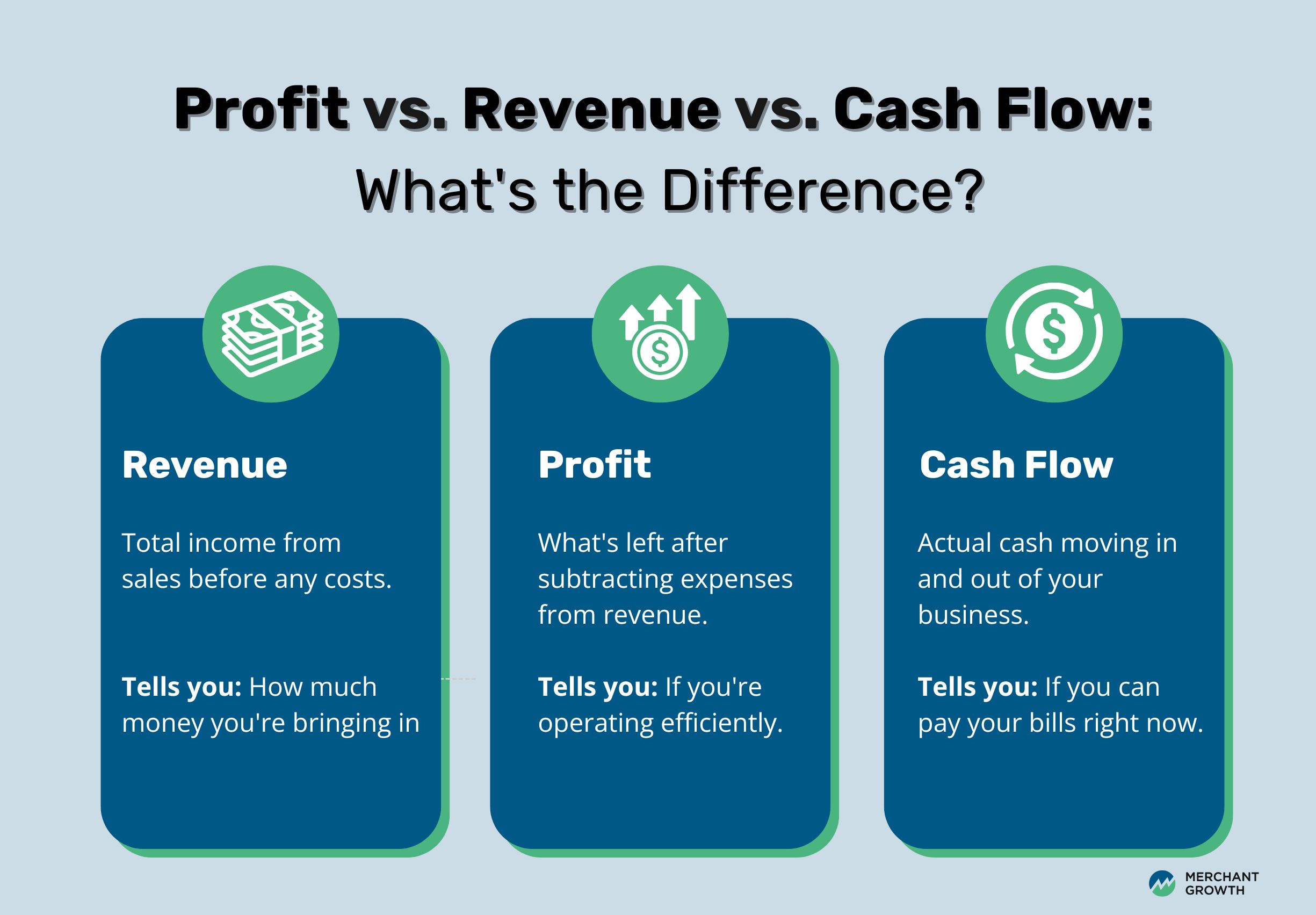

Cash Flow is Not the Same as Profit or Revenue

A business can show a profit on paper while still struggling to pay its bills because profit reflects what you have earned, not what you have collected. Revenue reports sales activity, while cash flow reflects what money is actually available to spend. Daily operations rely on cash, not accounting results, which is why understanding your cash flow is critical.

For Canadian small businesses, this becomes even more important. Many operate with seasonal sales cycles, longer payment windows, rising input costs, and supply chain delays. Without careful attention to how and when money moves, even strong businesses can find themselves squeezed at the wrong moment.

Good cash flow management sits at the centre of this. It involves tracking inflows and outflows regularly, planning for upcoming needs, and making strategic decisions to ensure your business always has enough liquidity to stay steady and take advantage of new opportunities. Whether you are budgeting for next quarter, preparing for a slower season, or planning the timing of a major purchase, a clear understanding of cash flow gives you the confidence to move forward without guesswork.

What Are the Key Aspects for Cash Flow Management?

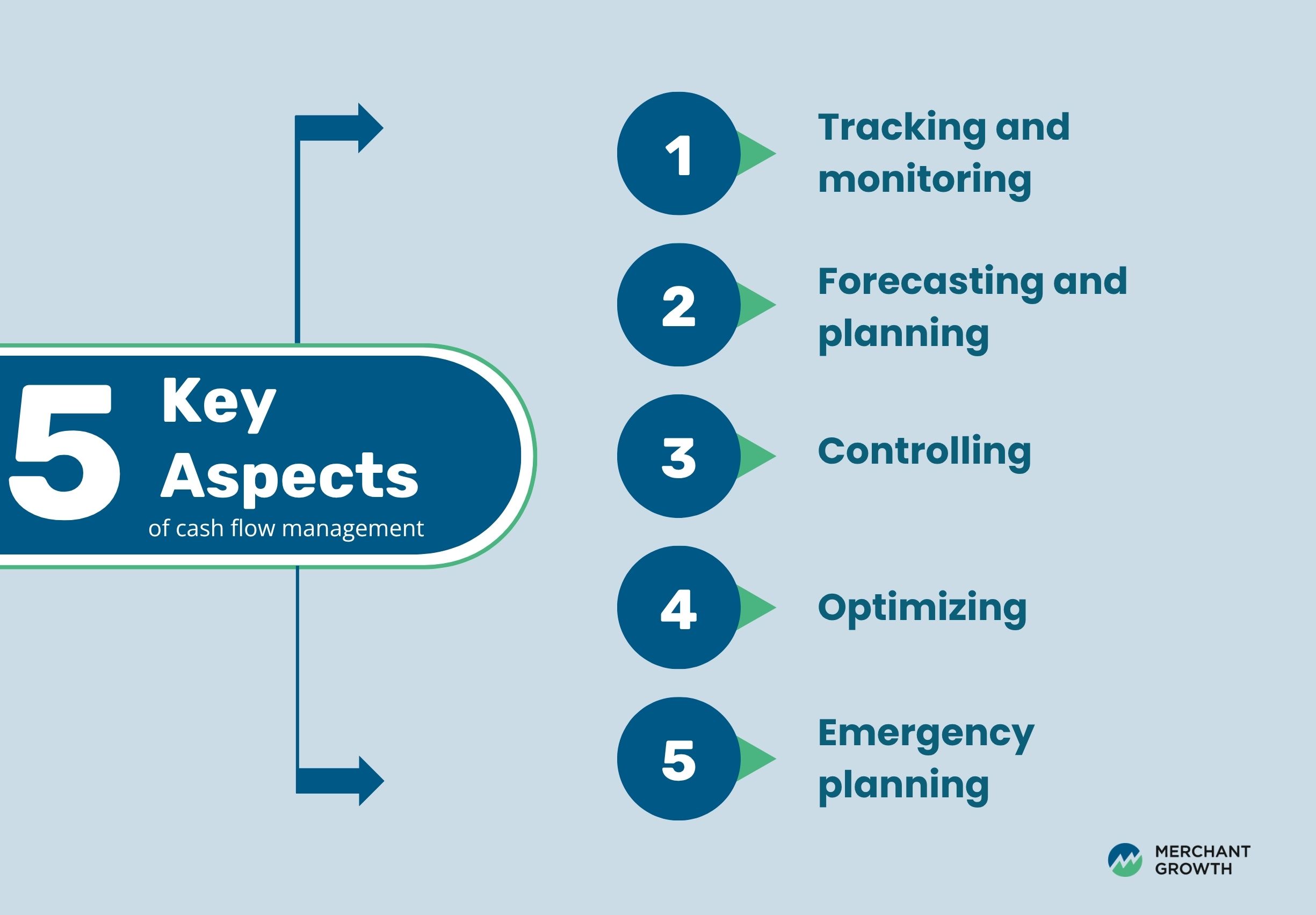

Mastering cash flow doesn’t happen by chance—it requires discipline, planning, and a proactive mindset. Successful business owners treat cash flow management as an ongoing practice, not just a financial report to glance at during tax season. By focusing on a few essential pillars, you can create a system that helps your business stay resilient in lean times and ready to grow when opportunity strikes.

Here are five foundational elements of strong cash flow management:

1. Tracking and monitoring

The first step in managing cash flow is knowing where your money is going—and when it’s arriving. Regularly tracking daily, weekly, and monthly cash movements allows you to stay ahead of any gaps, delays, or unexpected expenses. This isn’t just bookkeeping—it’s visibility. The more frequently you monitor your cash inflow and outflow, the better equipped you’ll be to make real-time adjustments and avoid unpleasant surprises.

Tip: Use cloud-based accounting tools or connect with a bookkeeper who can provide ongoing reports that show cash trends over time.

2. Forecasting and planning

Cash flow forecasting involves projecting your income and expenses over the weeks and months ahead. By using historical data and factoring in upcoming seasonal trends, large purchases, or potential slow periods, you can anticipate when cash might get tight and plan accordingly. Effective forecasting turns your finances from reactive to strategic, helping you avoid last-minute scrambles.

Tip: Build forecasts for multiple scenarios (e.g., best case, expected, and worst case) so you’re always prepared.

3. Controlling

Controlling your cash flow is about actively managing expenses and tightening up areas where money might be leaking. This means sticking to budgets, reviewing costs regularly, and keeping a close eye on payment terms. Ensure you’re not paying vendors faster than you’re being paid, and try to align outflows with inflows as closely as possible.

Tip: Implement approval processes for larger expenses and review recurring charges quarterly to trim unnecessary costs.

4. Optimizing

Optimization focuses on getting the most out of every dollar your business spends or earns. This can include renegotiating supplier contracts, improving your invoicing process to speed up payments, or incentivizing early customer payments. Small adjustments to operations or cash management processes can have a big impact over time.

Tip: Offer early payment discounts to clients and consider automating your billing system to avoid delays.

5. Emergency planning

No matter how well you plan, unexpected costs can and will arise—whether it’s a broken piece of equipment, a late-paying client, or a market downturn. Emergency cash flow planning involves setting aside a financial buffer or access to fast capital so you’re not caught off guard. This fund is your safety net, helping you cover urgent expenses without disrupting operations or going into high-interest debt.

Tip: Aim to build a contingency reserve equivalent to at least one month of operating expenses, and consider maintaining access to a line of credit for additional flexibility.

How Strong Cash Flow Supports a Healthy Business

Understanding cash flow is important, but knowing why it matters on a day-to-day basis is what truly empowers business owners. Healthy cash flow gives you the stability to handle challenges, the flexibility to grow, and the clarity to make confident financial decisions. When you manage cash flow intentionally, you create a business that feels less reactive and far more in control.

It Strengthens Financial Stability

Tracking inflows and outflows consistently helps you spot early warning signs such as rising expenses, slower customer payments, or declining revenue. When you catch issues early, you can adjust before they turn into real problems. This keeps essential obligations like payroll, rent, and supplier payments running smoothly.

It Supports Sustainable Growth

Growth requires resources. Whether you are hiring new employees, investing in equipment, or expanding into a new market, available cash gives you the freedom to move forward without taking on unnecessary debt. Strong cash flow opens the door to opportunities rather than limiting them.

It Prevents Financial Distress

Cash shortages can quickly lead to missed payments, penalties, damaged credit, and strained supplier relationships. If the pattern continues, the business may even face insolvency. Healthy cash flow helps you stay ahead of your obligations and avoid the stress that comes with constantly trying to catch up.

It Leads to Smarter Decision Making

When you clearly understand how money moves through your business, you can plan with intention. You can budget accurately, evaluate investments realistically, and prepare for slower periods instead of being surprised by them. This clarity turns decision making from reactive to strategic.

Strong cash flow forms the foundation for every other part of your financial planning. To manage it effectively, it helps to understand how cash flow is tracked and organized. Next, we will look at the cash flow statement and the categories that show where your money is coming from and where it is going.

Understanding Cash Flow Statements and Categories

A cash flow statement is one of the most powerful financial tools available to your business. It shows exactly how money moves in and out of your company and helps you understand how effectively you are generating, using, and preserving cash. For lenders and investors, it reveals whether the business is healthy and sustainable. For owners, it provides insight that supports better decisions about spending, saving, and planning.

A cash flow statement is divided into three main sections. Each section highlights a different part of your operations, and together they create a complete picture of your financial activity.

Operating Activities

Operating activities capture the cash generated or spent through your everyday business operations. This section reflects the financial strength of your core business model and is often the first place lenders and investors look when assessing performance. A healthy business typically shows positive operating cash flow because day-to-day activities bring in more cash than they consume.

Common items included in operating activities are the following.

- Cash received from sales of products or services

- Payments to suppliers for inventory or materials

- Employee wages and payroll expenses

- Rent, utilities, and office supplies

- Insurance premiums

- Income taxes paid

- Marketing and advertising costs

- Short-term software subscriptions

If a transaction is tied to your normal operations, it likely belongs in this category.

Investing Activities

Investing activities capture cash used to acquire or sell long-term assets. These transactions support the future direction or growth of your business. It is common for investing cash flow to be negative during periods of expansion, and in many cases that is a positive sign. For example, a retailer may show strong operating cash flow from healthy sales while also showing negative investing cash flow because they purchased new equipment or opened an additional location. This combination can signal strategic growth rather than financial strain.

Investing activities commonly include the following.

- Purchase or sale of property, equipment, or vehicles

- Investments in technology infrastructure or capitalized software

- Buying or selling shares in other companies

- Proceeds from selling long-term assets

Although these items do not appear frequently, they reveal how your business reinvests capital and prepares for the future.

Financing Activities

Financing activities show how your business raises money and how it repays those obligations. This section outlines your reliance on loans, equity, or owner contributions. It also shows how effectively you are managing your debt and funding structure.

Financing activities often include the following.

- Cash received from business loans, lines of credit, or merchant advances

- Equity investments from owners or shareholders

- Principal repayments on loans

- Owner withdrawals or shareholder dividends

- Repurchasing company shares

This section helps both owners and lenders understand how your business is funded and how responsibly it handles that financing.

Putting It All Together

When you review all three sections side by side, they reveal a story about the health and direction of your business. A company with strong operating cash flow and negative investing cash flow may be expanding wisely. A company with weak operating cash flow and high financing inflows may be relying too heavily on borrowed money to stay afloat. Understanding these patterns allows you to see what is working, what needs attention, and where your business is headed.

Accounting software makes reviewing your cash flow statement easier, but even with professional tools, it is important to interpret these sections regularly. This ensures you are making decisions based on actual liquidity, not just accounting profit.

The Five Cash Flow Categories

In addition to the three sections of the cash flow statement, it can be helpful to think about cash flow through five broader categories. These categories make it easier to analyze trends, uncover inefficiencies, and plan for future needs.

| Cash Flow Category | Definition |

|---|---|

| Operating cash flow | Cash generated from day-to-day operations such as sales and services. |

| Investing cash flow | Cash spent or received from buying or selling assets like property, equipment, or investments. |

| Financing cash flow | Cash from funding sources, including loans, equity investment, or repayments. |

| Net cash flow | The total amount of cash a business gains or loses over a specific period. |

| Future cash flow | Projected cash flow based on current operations and trends, used for planning ahead. |

Understanding these categories helps you see not only how cash moves today but also how it might move tomorrow. This clarity lays the foundation for stronger forecasting and more strategic cash flow management.

Key Cash Flow Metrics Every Business Should Track

Understanding your cash flow statement is a strong start, but the next step is knowing how to measure the speed and efficiency of your cash movement. This is where cash flow metrics come in. These numbers help you look beyond your bank balance and understand how quickly your business turns its investments into cash. When you track these metrics regularly, you can spot issues early and make small adjustments that lead to meaningful improvements.

Cash Conversion Cycle

The cash conversion cycle shows the amount of time it takes to turn your investment in inventory and other resources into cash from sales. It connects the full journey of your cash: how long money is tied up in inventory, how quickly that inventory sells, and how fast customers pay their invoices. A shorter cycle means your business recovers cash more quickly, which improves flexibility and gives you more room to make proactive decisions.

Days Sales Outstanding

Days Sales Outstanding measures how long it takes customers to pay you after receiving an invoice. A rising number is often a sign that your customers are paying more slowly than before, which can strain cash flow even if sales remain strong. Clear invoicing, automated reminders, and convenient payment options can significantly improve this metric and bring cash in faster.

Days Payables Outstanding

Days Payables Outstanding shows how long your business takes to pay suppliers. Extending this period, when done responsibly, helps you hold on to cash longer and smooth out timing gaps between payables and receivables. It is important to balance this metric with strong supplier relationships, since paying too slowly can affect trust and future terms.

Days Inventory Outstanding

Days Inventory Outstanding tracks how long inventory sits before it is sold. High numbers can indicate slow-moving products or excess stock, both of which tie up cash that could be used elsewhere in the business. Reducing this metric through better inventory planning or stronger forecasting helps free up capital and keeps your cash cycle moving.

These metrics offer a clearer view of how your business uses cash and where improvements can be made. When you understand them, you can make targeted adjustments that strengthen your financial position without dramatic operational changes. This sets the stage for more effective forecasting and smarter planning, which we explore next.

Forecasting and Scenario Planning

Forecasting is one of the most valuable tools for maintaining healthy cash flow. Instead of guessing what your financial position will look like next month or next quarter, forecasting helps you anticipate upcoming demands, prepare for slow periods, and make confident decisions based on real numbers. It turns cash flow management into a proactive process rather than a reactive one.

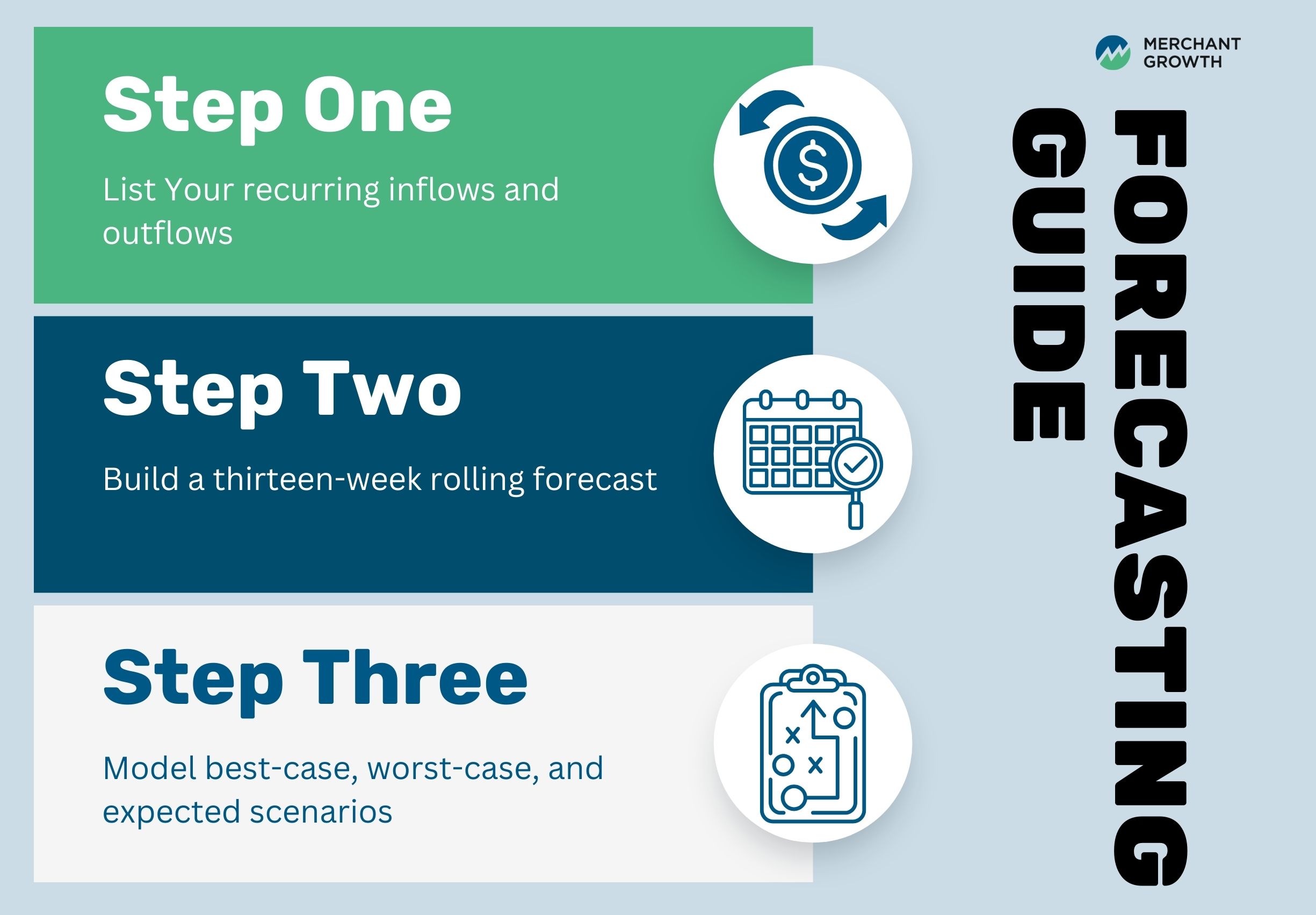

A strong forecast does not need to be complicated. What matters most is building a process that is consistent, easy to maintain, and based on reliable information. A thirteen-week rolling forecast is a common choice among accountants and financial advisors because it gives you enough visibility to stay ahead while still being flexible enough to update regularly.

Step One: List Your Recurring Inflows and Outflows

Begin by identifying every predictable movement of cash. This includes customer payments, subscription revenue, payroll, rent, supplier invoices, utilities, and loan repayments. Listing these items helps you build a baseline that reflects your regular financial rhythm.

At this stage, accuracy matters more than perfection. If a payment or expense recurs every month, include it. If revenue fluctuates seasonally, note that as well, since it will help you plan more effectively.

Step Two: Build a Thirteen-Week Rolling Forecast

Once you know your recurring inflows and outflows, map them across the next thirteen weeks. This timeline is long enough to anticipate upcoming obligations and short enough to update easily as new information comes in.

Your forecast should show how much cash you expect to have at the beginning of each week, how much will come in, how much will go out, and how much will remain at the end. As each week passes, add a new week to maintain the thirteen-week view. Over time, this rolling method creates a clear picture of patterns, challenges, and opportunities.

Step Three: Model Best-Case, Worst-Case, and Expected Scenarios

Forecasting becomes even more powerful when you explore different possibilities. Scenario planning helps you understand how your cash flow will respond to changes beyond your control, such as sales fluctuations, delayed customer payments, or unexpected expenses.

Your expected scenario reflects what is most likely to happen based on your current data.

Your best-case scenario could include stronger sales, faster customer payments, or reduced expenses.

Your worst-case scenario might explore slower revenue, a large unexpected cost, or a client paying later than usual.

Comparing these scenarios helps you prepare for challenges before they arise and take advantage of opportunities when conditions improve.

A Simple Example

Imagine a busy landscaping company heading into its slower winter season. Its thirteen-week forecast shows that revenue naturally declines in January and February. In a worst-case scenario, two major clients delay payments by three weeks. Without forecasting, this delay might lead to payroll stress or late supplier payments. With forecasting, the owner sees the shortfall coming and arranges a line of credit or adjusts spending to bridge the gap. What could have been a crisis becomes a manageable situation.

Using Automation for Better Forecasting

Modern accounting and cash flow tools can make forecasting even more accurate. Software that connects directly to your bank feeds, invoicing system, and payables can pull real-time data into your forecast. With automated updates, you can see the impact of new sales, delayed payments, or changing expenses immediately. This helps you make decisions quickly and maintain confidence in your financial planning.

Forecasting and scenario planning work together to give you visibility, control, and peace of mind. With clearer insight into what is coming, you can run your business with more stability and respond to challenges with confidence.

Practical Strategies to Improve Cash Flow

Managing cash flow effectively comes down to pulling a few key financial levers that influence how quickly money enters your business, how carefully it is spent, and how efficiently resources are managed inside your operation. These levers align directly with the core metrics you already track, including your cash conversion cycle, days sales outstanding, days payables outstanding, and days inventory outstanding. When you understand how each lever works, you can make small, targeted adjustments that lead to meaningful improvements in your cash position.

Improving Cash Inflows

Improving inflows begins with strengthening your receivables process. This is where your days’ sales outstanding plays a major role. The faster customers pay, the healthier your cash flow becomes.

Sending invoices immediately after work is completed, offering multiple payment options, and following up consistently all help reduce the time between completing a sale and receiving cash. Many businesses also see success by offering small incentives for early payments, such as a modest discount for paying within ten days. These tactics shorten your days’ sales outstanding and bring cash in sooner without sacrificing profitability.

You can also explore financial tools such as invoice financing or short-term credit to bridge temporary gaps. These solutions allow you to access cash based on outstanding invoices, which can be especially useful if your customers operate with longer payment terms.

Controlling Cash Outflows

Controlling outflows is equally important and closely tied to your days’ payables outstanding. Regularly reviewing your expenses helps you identify where you can reduce costs, negotiate better pricing, or adjust spending habits. Many suppliers are open to extending payment terms, and lengthening these timelines responsibly can help you hold on to cash longer while maintaining strong relationships.

Before making large purchases, consider whether leasing equipment, purchasing used, or phasing investments over time might support more stable cash flow. Small adjustments to how and when you spend can significantly ease pressure on your cash position.

Optimizing Working Capital

Working capital management has a direct impact on your cash conversion cycle. The faster you turn inventory into sales and sales into cash, the stronger your financial position becomes.

Reducing excess inventory is one of the most effective ways to free up cash. Whether that means ordering smaller quantities, improving your forecasting, or negotiating with suppliers for more frequent deliveries, the goal is to lower your days inventory outstanding. When inventory moves more quickly, you spend less time with cash tied up on the shelf.

Strategic use of credit can also support your working capital. A line of credit or short-term financing can help you cover temporary shortfalls, manage seasonal fluctuations, or take advantage of time-sensitive opportunities without disrupting daily operations.

Seeing Your Cash Levers as a System

These strategies work best when viewed as part of a larger system. Improving inflows reduces your days’ sales outstanding. Controlling outflows influences your days payables outstanding. Optimizing working capital strengthens your cash conversion cycle. Small improvements across these areas add up and create a more resilient and predictable cash flow.

With the right strategies in place, the next step is choosing tools that help you track performance, automate tasks, and make these processes easier to manage. That is where modern financial software can make a meaningful difference.

Tools, Software, and Automation

Technology can transform how you manage cash flow. Modern accounting and financial tools automate time-consuming tasks, reduce errors, and give you clearer visibility into your financial position.

Cloud-based accounting platforms such as QuickBooks, Xero, Wave, and Sage offer helpful features like automatic bank feeds, receipt scanning, and real-time reporting. AP and AR automation tools streamline payment processing, send invoice reminders, and provide alerts when due dates are approaching.

Dashboards and visualization tools allow you to see trends at a glance. Instead of sorting through spreadsheets, you can instantly understand whether your cash flow is improving or declining. These tools make daily financial management faster, more accurate, and significantly less stressful.

Cash Flow Analysis and Reviewing Results

Regular cash flow analysis gives you a deeper understanding of how your business is performing and helps you take corrective action before small issues turn into larger problems. For most small businesses, reviewing cash flow monthly is enough to stay confident and in control. Businesses with high transaction volumes may prefer weekly check-ins to maintain a closer watch.

Start your review by comparing your actual inflows and outflows to your forecast. Look for patterns such as delayed customer payments, rising expenses, or weaker-than-expected sales. These differences help you understand where adjustments may be needed and which assumptions should be updated going forward.

Once you have reviewed the timing of cash movement, take a closer look at your cash flow metrics. Improvements in areas such as days sales outstanding or days inventory outstanding can make an immediate difference in stability. These metrics give you a measurable way to evaluate whether your operational processes are moving in the right direction.

It is also helpful to understand how lenders and investors interpret your cash flow. They look at your numbers not only to assess performance but also to determine how well your business can handle debt. Two simple measures are especially important. Free cash flow shows how much cash your business has available after covering operating costs and necessary investments. This number indicates your capacity to grow, repay debt, or withstand unexpected expenses. The cash flow coverage ratio compares your cash flow to your debt obligations and reflects how comfortably you can make payments. A stronger ratio signals lower financial risk and greater borrowing power.

When your cash flow is steady and predictable, securing financing becomes easier. Lenders feel more confident, and your business gains access to the capital needed to bridge short-term gaps or support long-term expansion.

By making cash flow analysis a consistent part of your routine, you develop a clearer financial picture and the confidence to plan for growth rather than react to surprises.

Common Cash Flow Pitfalls and Risk Scenarios

Even with strong habits and thoughtful planning, cash flow challenges can still appear when certain business practices slip under the radar. Recognizing these issues early makes it much easier to stay financially steady and avoid unnecessary stress. Here are some of the most common cash flow pitfalls small and growing businesses face, along with why they matter.

Rapid Business Growth and Expansion

Growth is exciting, but scaling too quickly can strain your finances. New hires, inventory purchases, marketing campaigns, and equipment upgrades often require significant cash upfront. If revenue does not arrive fast enough to offset these costs, your business can become overextended. Even healthy sales numbers cannot compensate for a cash gap if expenses rise faster than inflows. Thoughtful planning and clear financial projections help ensure your growth is sustainable rather than overwhelming.

Lack of Organization in Accounts Receivable

One of the fastest ways to weaken cash flow is to let receivables pile up. When invoices go out late, follow-ups are inconsistent, or overdue accounts are not monitored, money you have already earned sits uncollected. Disorganized accounts receivable processes can leave you short on cash even during strong sales periods. A structured invoicing system, timely reminders, and clear payment expectations help keep cash flowing in when it should.

Extending Credit Without Safeguards

Offering payment terms can attract customers and close deals, but it also shifts risk onto your business. Without basic safeguards like credit checks, limits, or deposit requirements, too much capital can become tied up in unpaid invoices. This leaves your business covering its own expenses while waiting on customer payments. A well-managed credit policy protects your cash flow while still giving customers flexibility.

Difficulty Projecting Expenses

Unexpected costs are unavoidable, but failing to anticipate them can disrupt your cash flow quickly. Many businesses underestimate recurring expenses such as tax instalments, equipment maintenance, or seasonal slowdowns. Others forget to set aside funds for unplanned repairs or emergencies. A reliable forecast that includes both predictable expenses and a buffer for surprises helps your business stay steady even when something unexpected comes up.

How Lenders and Investors View Cash Flow

When lenders and investors evaluate a business, cash flow is often the first thing they look at. It tells them, in practical terms, whether your business can pay its bills, handle new debt, and continue operating smoothly. While profit matters, cash flow reveals your real financial strength and day-to-day stability.

Lenders use cash flow to assess creditworthiness because it shows how much money your business consistently generates and how reliably you can cover obligations like loan payments, payroll, and supplier invoices. Strong, predictable cash flow signals lower risk, which can improve your chances of securing financing and even help you negotiate better terms.

Two measurements are especially important. Free cash flow represents the money left after covering operating expenses and necessary investments like equipment. It shows how much cash you have available for growth, savings, or debt repayment. The cash flow coverage ratio compares your available cash to your debt payments. A higher ratio tells lenders you have more than enough cash to meet your obligations, which increases their confidence in your financial stability.

When your cash flow is healthy, accessing funding becomes much easier. Lenders are more willing to support your plans, and investors view your business as capable of sustaining growth. This is also where flexible financing partners, like Merchant Growth, can play an important role by helping businesses smooth out cash flow gaps, manage seasonal swings, or take advantage of strategic opportunities.

Understanding how external stakeholders interpret your cash flow puts you in a stronger position when seeking support and helps you address any weaknesses before applying for financing.

Financing for Cash Flow Management

Financing can play a meaningful role in keeping your cash flow healthy, especially during slower seasons, unexpected dips in revenue, or moments when large expenses land all at once. Instead of draining your cash reserves to cover operating costs or make strategic purchases, the right financing can give you the breathing room you need to stay steady. Tools like a line of credit or short-term loan help bridge temporary gaps, support predictable operations, and let you take advantage of growth opportunities without putting pressure on your day-to-day budget. The key is choosing a financing option that complements your broader financial strategy rather than adding strain.

Line of credit

A business line of credit offers flexible access to funds whenever you need them. It’s a practical way to smooth out cash flow swings, cover short-term expenses, or take advantage of unexpected opportunities. By giving you the ability to draw and repay funds as needed, a line of credit can help you avoid late payment fees, maintain strong supplier relationships, and keep operations running smoothly.

Invoice factoring

Invoice factoring improves cash flow by turning unpaid invoices into immediate working capital. Instead of waiting weeks or months for customers to pay, you can access a portion of that cash right away. This reduces reliance on collections, stabilizes inflows, and allows you to offer competitive payment terms without weakening your cash position. Since it is not a loan, it also avoids adding new debt to your balance sheet.

Term financing

Term financing provides an upfront lump sum based on projected future sales, including credit and debit card revenue. This type of funding is typically easier to qualify for, does not require collateral, and offers repayment schedules that adjust alongside your cash flow. For many businesses, this flexibility makes planning easier and provides a more predictable financial path forward.

Strategic use of financing can be the difference between pausing progress and moving ahead with confidence. Whether you are preparing for a busy season, upgrading equipment, or smoothing out uneven revenue cycles, access to flexible capital supports your ability to grow without disrupting everyday operations. If you are considering how financing fits into your cash flow plan, these options are a great place to begin exploring what works best for your business.

How Merchant Growth Helps Businesses Manage Cash Flow

Even with strong planning and systems in place, many small businesses experience cash flow gaps due to slow receivables, seasonal fluctuations, or unexpected expenses. Merchant Growth provides flexible funding solutions that can help you bridge these periods, invest in new opportunities, or build a buffer for future challenges.

Working capital loans and revenue-based financing can support inventory purchases, equipment upgrades, digital improvements, and other initiatives that strengthen your business. By pairing smart cash flow management with the right financing tools, you give your business the stability it needs to grow with confidence.

If you are looking to strengthen your cash flow or prepare for your next stage of growth, Merchant Growth can help you find the right solution for your goals.