Running a small business in Canada means juggling a thousand moving parts at once, including sales, staff, suppliers, rent, and of course, taxes. Even profitable, well run businesses can find themselves behind on GST/HST, payroll deductions, or corporate income tax when cash flow tightens, a major client pays late, or expenses spike unexpectedly.

When a brown envelope from the Canada Revenue Agency (CRA) arrives, it can feel overwhelming. Words like arrears, collections, and enforcement can quickly trigger fears about frozen bank accounts, liens, or wage garnishments. But there is an important truth many business owners do not realize. CRA payment plans exist because tax debt is common, not because businesses have failed.

This article is here to help you make sense of what is happening and what your options are. We will walk through how CRA payment plans work, who qualifies, what they cost, and how to decide whether one fits your situation, so you can move forward with confidence instead of anxiety.

Key Takeaways

- CRA payment plans allow businesses to repay tax debt over time instead of all at once.

- Interest still applies, but payment plans can prevent aggressive collection actions.

- Setting up a plan early improves approval chances and flexibility.

- Payment plans are not one size fits all. The best option depends on your cash flow and long term viability.

- The right strategy balances CRA compliance with business survival and growth.

What Is a CRA Payment Plan and When Businesses Use Them

A CRA payment plan, officially called a payment arrangement, is a formal agreement between your business and the CRA that allows you to pay off tax debt in manageable monthly installments instead of all at once.

These plans are most commonly used when a business owes:

- GST/HST

- Payroll deductions for employees

- Corporate income tax

What matters most to the CRA is not just how much you owe, but what you can realistically afford. Instead of focusing on the total balance, they look at a more human and practical question: how much can this business reasonably pay each month while still staying afloat?

If paying your full balance right now would cause serious financial strain or make it difficult to keep your doors open, the CRA will often work with you. Many business owners are surprised by how flexible the process can be when they come forward honestly and show they want to get back on track.

Why CRA Payment Plans Are Often the Preferred Path

The CRA’s goal is to collect what is owed, not to shut down businesses that are trying to do the right thing. When owners communicate early and stay engaged, the CRA is usually far more interested in working together than taking aggressive action.

Payment plans allow the CRA to recover tax revenue in a steady, predictable way, while allowing businesses to keep operating, paying staff, and serving customers. That balance matters. From the CRA’s perspective, a business that is still running and generating income is far more likely to repay its tax debt than one that has been pushed into crisis.

For business owners, this means that reaching out and setting up a plan is often the best way to replace fear and uncertainty with something far more useful: a clear path forward.

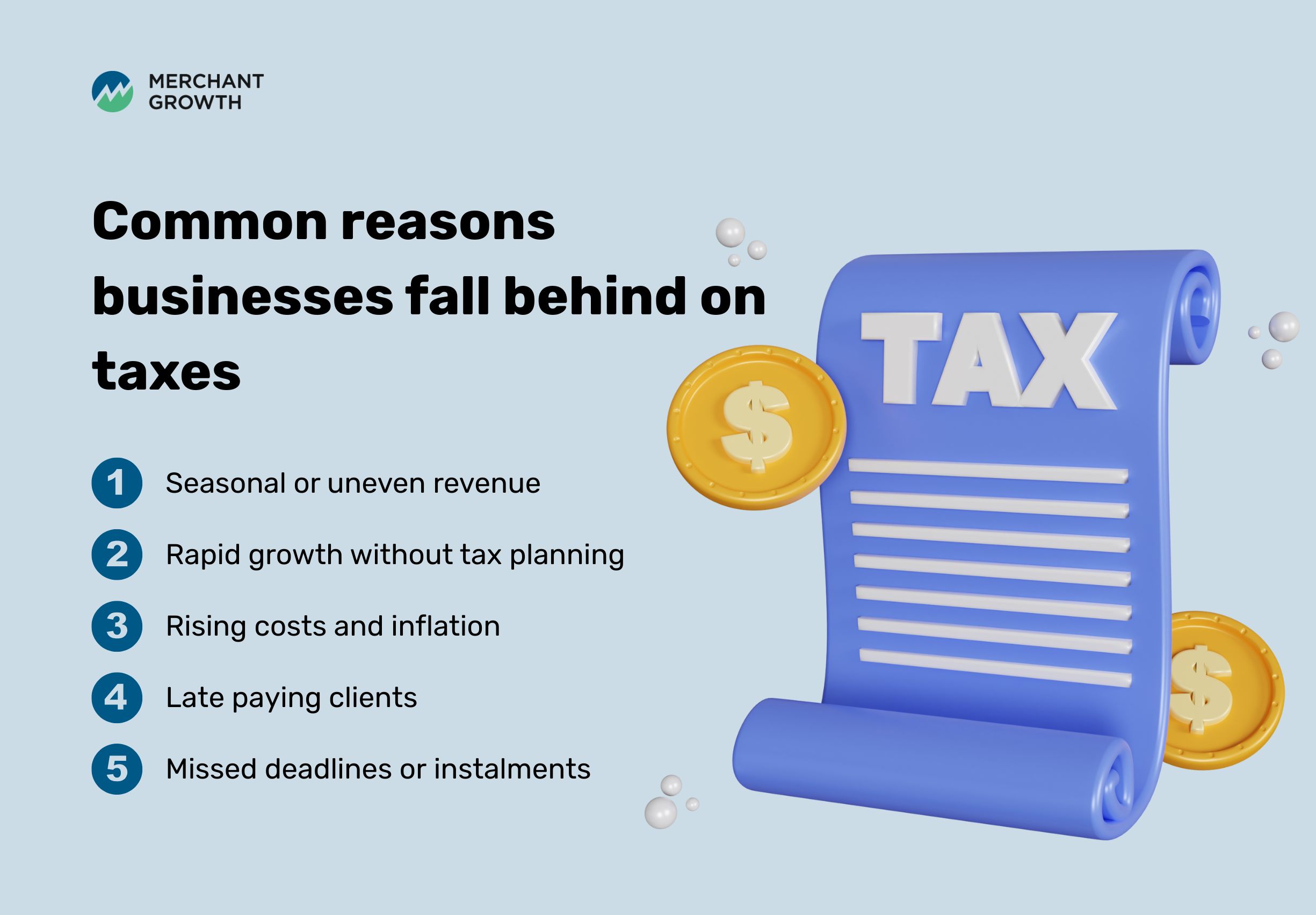

Why Small Businesses Often Fall Behind on CRA Taxes

Falling behind on taxes rarely means a business is poorly run. More often, it reflects how unpredictable cash flow can be, especially for small and growing companies that do not have large financial cushions. When income fluctuates, expenses keep coming, and customers pay on their own timelines, it becomes very easy for tax obligations to slip out of sync with reality.

What makes this especially stressful is that CRA deadlines do not adjust for slow months, late payments, or unexpected expenses. Even responsible, hardworking business owners can suddenly find themselves behind simply because the timing did not line up.

Here are some of the most common reasons it happens.

Seasonal or Uneven Revenue

Many Canadian businesses earn most of their income during specific times of the year. Construction companies, landscaping businesses, tourism operators, and retailers all experience these ups and downs. During peak season, revenue can be strong, but when things slow down, cash flow often tightens quickly. If a GST or payroll deadline lands during a quieter period, there may not be enough cash on hand to cover it, even if the business is doing well overall. This mismatch between when money comes in and when taxes are due is one of the most common reasons seasonal businesses fall behind.

Rapid Growth Without Tax Planning

Growth is exciting, but it can also be risky if it is not paired with careful tax planning. As sales increase, GST/HST collected increases too, and payroll obligations grow as you hire more staff. If those amounts are not being set aside consistently, they can start to pile up in the background. Many business owners do not realize how much they owe until a large balance suddenly appears, often at the worst possible time. What looks like success on the surface can quietly turn into tax stress behind the scenes.

Rising Costs and Inflation

Rent, wages, utilities, insurance, and inventory all cost more than they did just a few years ago. Even businesses with steady sales can struggle when expenses rise faster than revenue. When margins get squeezed, owners are often forced to choose between paying suppliers, covering payroll, or keeping the lights on. Taxes, unfortunately, can fall down the priority list during these periods, even when there is every intention to catch up later.

Late Paying Clients

You may have completed the work, delivered the product, and sent the invoice, but if your customer pays late, your tax obligation still arrives on time. This gap between when you earn money and when you actually receive it creates serious strain. It is one of the biggest drivers of short-term tax debt for small businesses, especially those that rely on a few large clients or long payment cycles.

Missed Deadlines or Installments

CRA deadlines and installment requirements are not always intuitive, particularly for newer business owners. A missed payment, a misunderstood installment, or a late filing can quickly turn into penalties and interest that make the balance grow faster than expected. What starts as a small oversight can snowball into something much harder to manage.

The most important takeaway is this. Tax debt is usually about timing, not character. Most business owners who owe the CRA are doing their best in a system that does not always line up neatly with real-world cash flow.

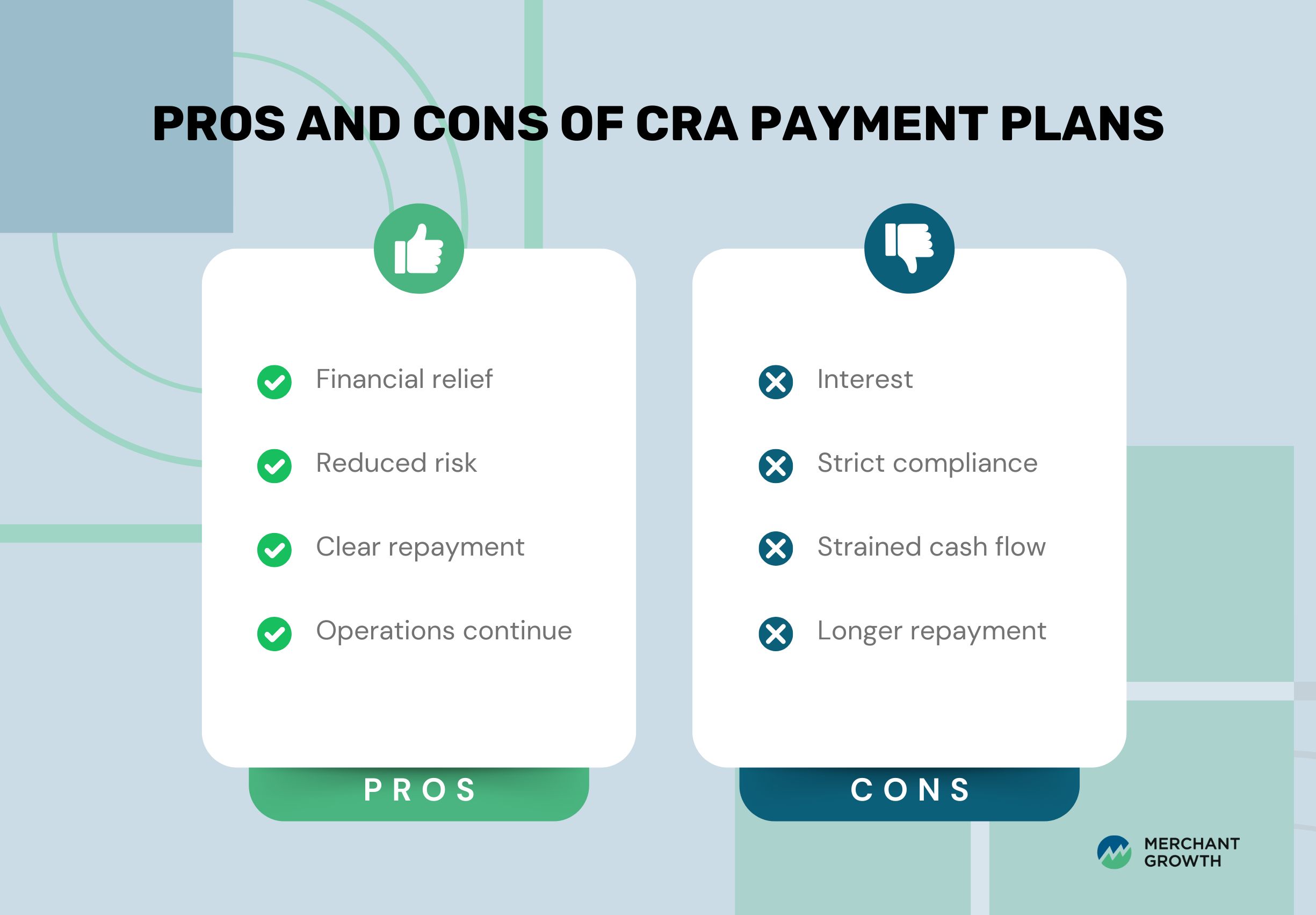

Pros and Cons of CRA Payment Plans for Small Businesses

CRA payment plans can be an important lifeline for businesses that need breathing room, but like any financial tool, they come with both benefits and limitations. Understanding both sides helps you make a choice that supports your business rather than simply postponing a problem.

The Benefits

When tax debt feels overwhelming, a payment plan can provide immediate relief by breaking a large balance into smaller, more manageable payments. This reduces the pressure to come up with a lump sum and helps stabilize cash flow, which allows you to keep paying employees, suppliers, rent, and other essential expenses.

Payment plans also lower the risk of disruptive CRA enforcement actions like frozen bank accounts or garnishments. Instead of worrying about what might happen next, you have a clear agreement in place and know exactly what is expected of you each month.

Some of the key benefits include:

- Immediate cash flow relief by spreading payments over time

- Reduced risk of enforcement, such as bank freezes or garnishments

- A clear repayment structure that makes planning easier

- The ability to keep operating while paying down tax debt

For many business owners, simply having a plan in place brings a huge sense of emotional relief. It replaces uncertainty with a sense of control and forward momentum.

The Limitations

At the same time, payment plans are not free. Interest continues to accrue until the balance is fully paid, which means long repayment periods can become expensive. You also need to stay fully compliant. All new tax obligations must be paid on time, or the CRA can cancel the agreement.

Even a reasonable monthly payment can put pressure on cash flow if your business is already tight. Over time, this can create ongoing stress and make it harder to invest in growth or recovery.

Some of the main drawbacks include:

- Interest continues to accrue until the balance is paid

- Strict compliance is required for new taxes

- Monthly payments may strain cash flow

- Longer repayment periods increase the total cost

A CRA payment plan can be helpful, but it is not always the most affordable or flexible solution. It should be chosen carefully, based on what your business can truly sustain.

Does CRA Charge Interest on Payment Plans?

Yes, the CRA charges interest on outstanding balances, even when you are on a payment plan. This surprises many business owners, but it is an important part of understanding the true cost of a long term arrangement.

Once a payment plan is in place, late payment penalties may stop, but interest usually continues to build until the balance reaches zero. That means the longer it takes to pay off your debt, the more it will cost in total.

This is why the goal is not just to get approved for a plan, but to find one that fits your business in a healthy way. A plan that stretches payments too thin may feel easier in the moment, but it can quietly increase the total amount you owe. A balanced approach protects both your cash flow and your long term financial health.

How to Set Up a CRA Payment Plan

Setting up a CRA payment plan is often far less intimidating than it sounds, especially when you break it into manageable steps. The key is to be organized, honest, and proactive.

Step 1: File All Outstanding Returns

Before the CRA will consider any payment arrangement, all required GST/HST, payroll, and corporate tax returns must be filed. Even if you cannot pay yet, filing shows that you are taking responsibility and working toward compliance. It also gives the CRA a clear picture of what is owed, which is essential for setting up a plan.

Step 2: Review What You Owe

Once your filings are up to date, review your balances through your CRA My Business Account or by speaking with the CRA directly. Look at how much is owed for each tax type so there are no surprises. This step gives you the foundation you need to build a realistic repayment plan.

Step 3: Assess What You Can Afford

This is one of the most important steps. Look closely at your monthly cash flow, including revenue, fixed expenses, and seasonal fluctuations. The goal is to choose a payment amount that actually moves your debt down without pushing your business into crisis. Overpromising here can lead to missed payments and more stress later.

Step 4: Apply

You can apply online through CRA My Business Account or by calling CRA collections. In either case, you will propose a payment amount and schedule. The CRA may accept it as is or suggest adjustments based on your financial information.

Step 5: Provide Financial Information

The CRA may ask for bank statements, revenue reports, or expense details to confirm what your business can afford. This is not meant to be punitive. It helps them ensure the plan is realistic and sustainable.

Step 6: Stay Compliant

Once your payment plan is approved, staying on track is critical. Make every payment on time and keep all new tax filings and payments current. This protects your agreement and keeps you out of collections.

Reaching out early and staying engaged gives you more flexibility and makes the entire process smoother.

When a CRA Payment Plan May Not Be the Best Option

CRA payment plans can help many businesses, but they are not always the right solution. The goal is not just to satisfy the CRA, but to do so in a way that keeps your business healthy.

A payment plan may not be a good fit if:

- Monthly payments leave you unable to cover payroll, rent, or suppliers

- Interest costs are growing faster than you can reduce the balance

- You need short term liquidity just to keep operating

- Tax debt is masking deeper cash flow or profitability issues

In these situations, a payment plan can quietly make things worse instead of better. If your business is struggling to survive, locking into payments that drain your remaining cash may only accelerate the problem.

The purpose of any repayment strategy should be to support your business and give it room to recover, not slowly starve it of the cash it needs to stay alive.

CRA Payment Plans vs. Other Ways to Manage Business Tax Debt

A CRA payment plan is only one way to deal with tax debt. Depending on your situation, other approaches may be more effective and less stressful.

Payment Plans and Short-Term Financing

Financing can allow you to pay the CRA in full right away, which stops interest and removes the threat of enforcement. You then repay the loan on terms that may be more flexible and predictable than a CRA plan, especially if your revenue fluctuates.

Payment Plans and Lump Sum Strategies

Some businesses use financing, refinancing, or even asset sales to settle their CRA balance quickly. While this requires a larger upfront payment, it can significantly reduce the total amount of interest paid and provide a clean slate.

Payment Plans and Cash Flow Restructuring

Improving how you invoice, speeding up collections, or renegotiating supplier terms can free up cash that allows you to pay CRA more aggressively. In some cases, these changes make it possible to clear tax debt faster without borrowing.

The best choice depends on your numbers, your timeline, and the overall health of your business, not just the size of your CRA balance.

A Healthier Way to Think About CRA Payment Plans

Instead of asking whether you can get a payment plan, it is more helpful to ask whether that plan will actually support your business. The right strategy should reduce stress, protect cash flow, and give you confidence that your company can continue operating and growing.

When payment plans are used thoughtfully, they become part of a larger recovery process. They allow you to deal with CRA debt in a way that fits your real financial situation instead of forcing your business into an unsustainable corner.

When tax debt is handled with a clear strategy, it becomes something you can manage and move past. It stops being a constant source of anxiety and becomes just one step on the path back to stability.

From CRA Stress to Financial Stability, How Merchant Growth Can Help

A CRA payment plan can stop collections, but it does not solve cash flow on its own.

Merchant Growth works with Canadian small businesses to help regain control of cash flow, pay CRA strategically, and avoid compounding financial stress.

With fast, flexible financing designed around real-world business realities, Merchant Growth can help you clear tax debt in a way that supports your future, not undermines it.

Take the Next Step

If CRA debt is weighing on your business, you do not have to navigate it alone. Talk to Merchant Growth about solutions that support repayment without sacrificing your business’s future.

You built your business to grow, not to be buried under tax stress. There is a path forward.