If you run a small business, you already know that money never moves in a straight line. Some months are strong, some are slow, and expenses never seem to wait. When an income tax deadline arrives in the middle of that, it can feel like one more thing landing at the worst possible time, even when your business is doing well.

What makes this even harder is that the income tax deadline for small businesses in Canada is not the same for everyone. Sole proprietors, partnerships, and corporations all follow different rules. On top of that, filing deadlines and payment deadlines are rarely the same date, which creates confusion, penalties, and unnecessary stress.

We will walk through the key dates, the forms you need, and how to plan for tax season so it fits into your cash flow instead of disrupting it.

Key Takeaways

- Small business income tax deadlines depend on whether you are a sole proprietor, partnership, or corporation

- Filing deadlines and payment deadlines are often different

- Sole proprietors usually file later but may owe taxes earlier

- Corporations must file within six months of their year-end, even if they cannot pay in full

- Planning ahead reduces penalties, interest, and financial strain

Filing Income Tax as a Sole Proprietor or Partnership

If you run your business as a sole proprietor or in a partnership, your business income is reported on your personal tax return. This setup is simple, but it is also where a lot of small business tax confusion starts. Because your business and personal taxes are filed together, it is easy to assume that all the deadlines line up. In reality, the CRA separates when you must file from when you must pay, which can catch even experienced business owners off guard.

Understanding how these dates work helps you avoid interest, penalties, and unnecessary stress.

Filing Your Return

Most self-employed Canadians have until June 15 to file their personal income tax return. If June 15 falls on a weekend or holiday, the deadline moves to the next business day. This later filing deadline exists because business owners need more time to finalize their income and expenses, especially if they do their own bookkeeping or work with an accountant.

However, this extra time to file often creates a false sense of security, because it does not mean you also have extra time to pay.

Paying What You Owe

Even though you can file in June, any income tax you owe is usually due by April 30. If you miss this payment date, interest starts accumulating immediately, even if your return is not due for another six weeks.

This is the most common and costly mistake sole proprietors make. Many business owners file on time in June but still get charged interest because they did not pay in April. The CRA treats filing and payment as two separate obligations.

Reporting Your Business Income

Your business income is reported using a business income schedule that is attached to your personal tax return. This form details your business revenue, expenses, and net profit, which is then added to your other personal income and taxed accordingly.

Because everything flows through your personal return, your business performance directly affects your personal tax bill. That is why estimating what you owe before April 30 is so important.

Important Dates for Sole Proprietors (2025 and ongoing)

- April 30: Payment deadline for any income tax owed

- June 15: Filing deadline for self-employed personal tax returns

- If June 15 falls on a weekend, the deadline moves to the next business day

Important Forms for Sole Proprietors

- Personal income tax return (T1)

- Business income schedule reporting revenue, expenses, and net profit

Income Tax Deadline for Incorporated Small Businesses

When your business is incorporated, it becomes its own legal and tax-paying entity. That means it has its own income tax return, its own deadlines, and its own payment schedule. These timelines are very different from those for sole proprietors, which is why incorporated business owners often feel surprised when tax payments are due much sooner than expected.

Understanding these differences makes it much easier to plan for tax time without disrupting your cash flow.

Filing Your Corporate Tax Return

Every corporation must file a corporate income tax return, even if the business was not active or did not make a profit. The filing deadline is six months after the end of your corporation’s fiscal year. For example, if your year-end is December 31, your filing deadline for the 2025 tax year would be June 30, 2026.

Filing on time is critical. Late-filing penalties can apply even if you eventually pay what you owe, so submitting the return by the deadline should always be a priority.

Paying Corporate Income Tax

Most small corporations must pay their income tax within two or three months after the end of their fiscal year, depending on whether they qualify for the small business deduction. This means the payment is usually due long before the tax return itself.

This gap between payment and filing deadlines often catches business owners off guard. If cash is not set aside throughout the year, the tax bill can arrive at a very inconvenient time.

Reporting Corporate Income

Corporations report their income, expenses, and tax owing on a T2 corporate income tax return. This return is separate from the owner’s personal tax return and must be filed even if the corporation had little or no activity.

Because corporate taxes are separate from personal taxes, business owners often need to plan for both, especially if they pay themselves through dividends or salary.

Important Dates for Corporations (2025 and ongoing)

- Two or three months after year-end: Corporate income tax payment deadline

- Six months after year-end: Corporate income tax return filing deadline

For a December 31 year-end, this typically means:

- Payment due by February 28 or March 31

- Return due by June 30

Important Forms for Corporations

- T2 corporate income tax return

- Financial statements showing revenue and expenses

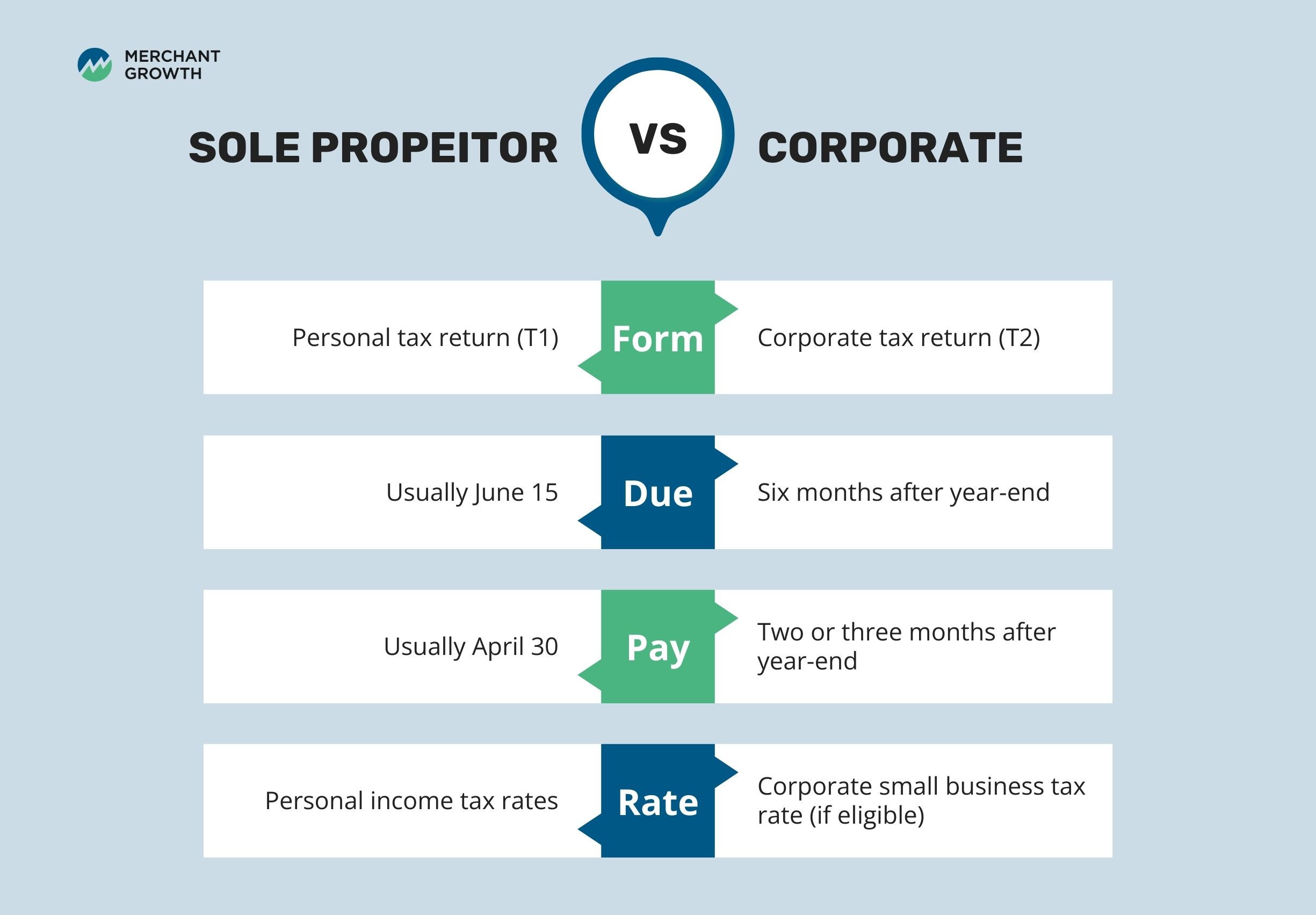

Key Differences Between Sole Proprietor and Corporate Tax Deadlines

One of the most important things to understand about small business taxes in Canada is that your business structure controls your tax calendar. Two businesses can earn the same amount of money, but face very different filing and payment deadlines simply because one is a sole proprietorship and the other is incorporated. This difference affects everything from cash-flow planning to how much time you have to prepare for a tax bill.

This table helps you quickly compare tax obligations for different business structures, so you can plan your filings and payments with confidence.

Seeing the deadlines side by side makes it much easier to understand how these systems work.

| Category | Sole Proprietor / Partnership | Corporation |

|---|---|---|

| Tax return filed on | Personal tax return (T1) | Corporate tax return (T2) |

| Filing deadline | Usually June 15 | Six months after year-end |

| Payment deadline | Usually April 30 | Two or three months after year-end |

| Tax rate applied | Personal income tax rates | Corporate small business tax rate (if eligible) |

What this table really shows is how timing shifts when you incorporate. Sole proprietors get more time to file but must pay earlier, while corporations have more time to file paperwork but much less time to pay the tax itself. That can create very different cash-flow pressures depending on how your business is structured.

Understanding these differences allows you to plan more intelligently. When you know when money has to leave your business, you can decide how much to set aside, when to collect receivables, and whether you need short-term funding to stay comfortable. The deadlines do not have to be stressful if they are built into your financial strategy.

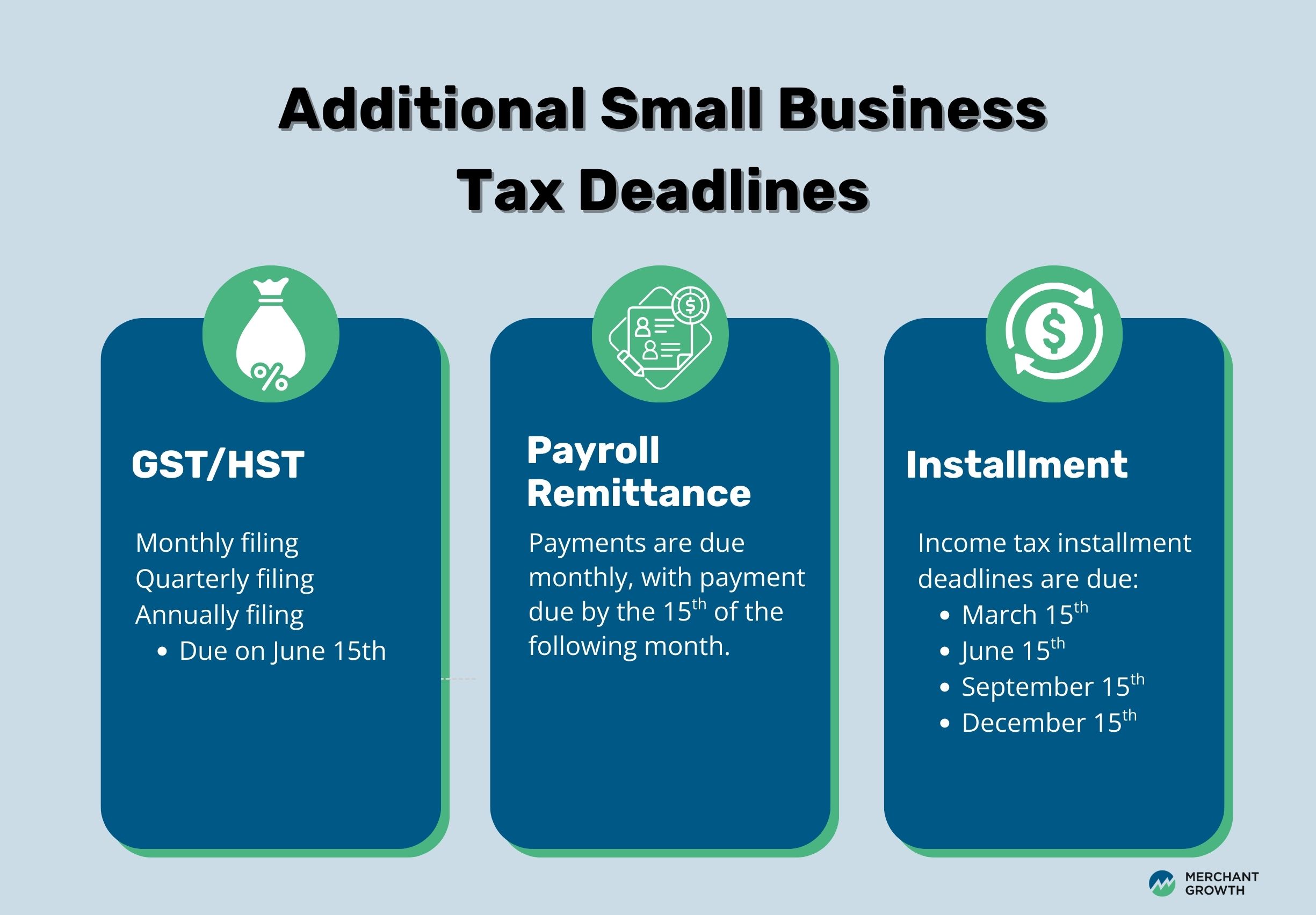

Small Business Tax Deadlines Beyond Income Tax

Income tax is only one part of what the CRA expects from small businesses. Many owners are also responsible for GST or HST filings, payroll remittances, and income tax installments. These obligations often come due around the same time, which can create real pressure on cash flow if they are not planned for in advance.

Understanding these dates helps you avoid the kind of surprises that lead to penalties, interest, and growing CRA balances.

GST and HST Filing Deadlines

How often you file your GST or HST return depends on your business, but most small businesses fall into one of these categories:

- Monthly filers must file and pay by the end of the month following the reporting period

- Quarterly filers must file and pay one month after the end of the quarter

- Annual filers usually must file and pay by June 15, but any amount owing is typically due by April 30

These deadlines often overlap with income tax season, which is why many businesses feel squeezed in the spring.

Payroll Remittance Deadlines

If you have employees, you must remit payroll deductions to the CRA. Most small businesses remit monthly, with payments due by the 15th of the following month. Some businesses remit more frequently depending on payroll size.

Missing a payroll remittance is taken seriously by the CRA and can result in immediate penalties and interest.

Income Tax Installment Deadlines

Many small business owners and corporations are required to make income tax installments throughout the year. These are advance payments toward your annual tax bill.

For most individuals and corporations, installments are due on:

- March 15

- June 15

- September 15

- December 15

If you skip installments or underpay them, you can face interest even if you pay your full tax balance later.

Common Mistakes Small Businesses Make Around Tax Deadlines

Most small business owners do not get into trouble with the CRA because they were careless or irresponsible. They get into trouble because the rules around tax deadlines are complicated, and those rules do not always line up with how cash actually moves through a business. When you are focused on customers, staff, and day-to-day operations, it is easy for tax obligations to feel secondary until a deadline suddenly arrives.

The patterns behind CRA penalties are remarkably consistent. In most cases, the same misunderstandings come up again and again.

Common mistakes include:

- Assuming that filing later means paying later

- Waiting until tax time to calculate what is owed

- Forgetting about installment payments

- Not setting aside money during the year

- Underestimating tax because deductions were missed

These mistakes almost always lead to the same outcome. The deadline arrives, the balance is higher than expected, and there is not enough cash on hand to pay it comfortably. The good news is that none of this is about bad intent. With clearer information and earlier planning, most of these problems are completely avoidable.

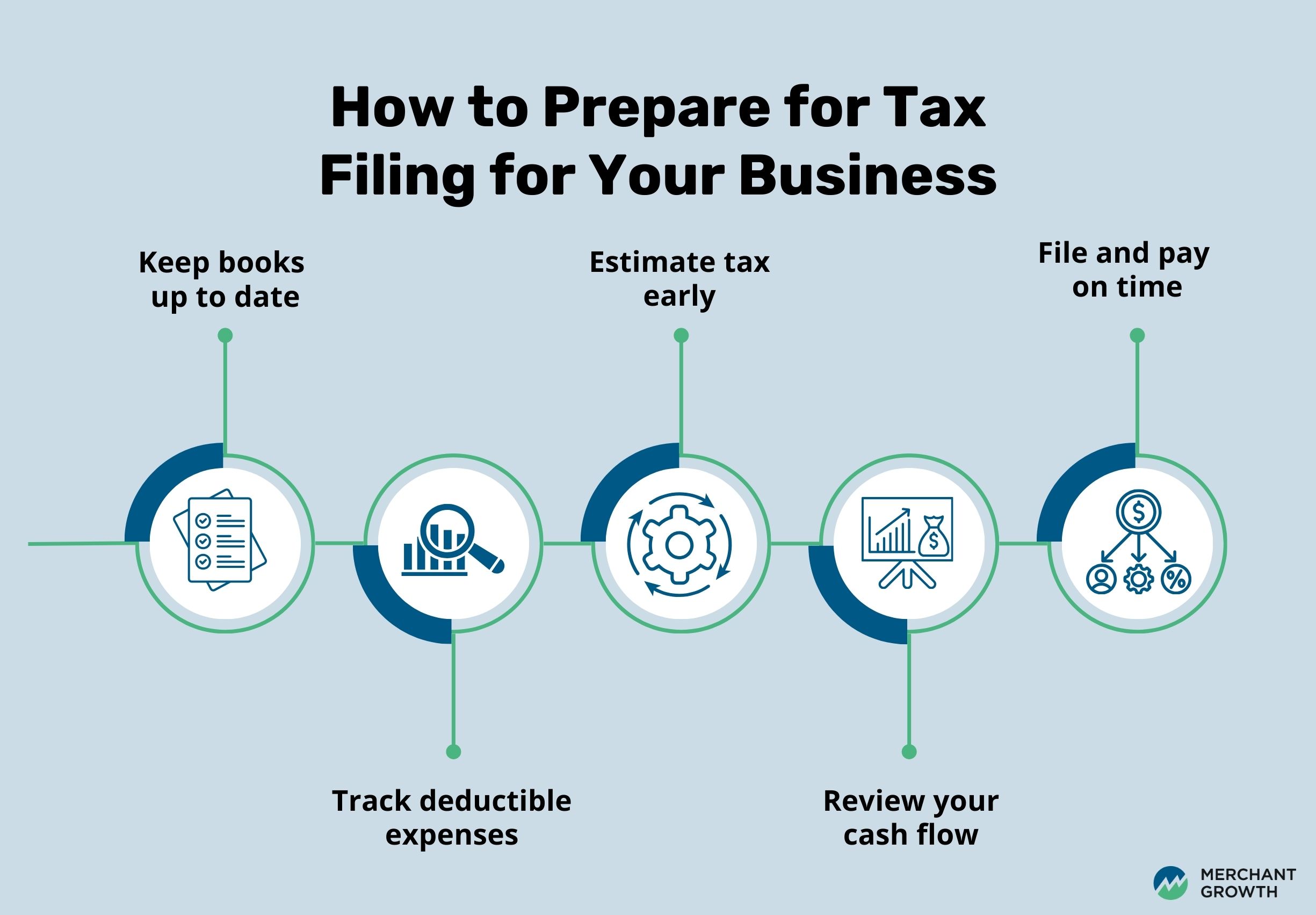

How to Prepare for Small Business Income Tax Filing

Preparing for your small business income tax return is not something that should start a week before the deadline. The less you rush, the less stressful and expensive tax season becomes. When you treat tax preparation as an ongoing process instead of a last-minute task, you give yourself more control over cash flow, more visibility into what you owe, and more options if you need flexibility.

Here is how to approach it step by step.

Step 1: Keep your bookkeeping up to date

Accurate bookkeeping is the foundation of everything else. When your books are current, you always know how much money is coming in, how much is going out, and what your profit looks like. This makes it much easier to estimate how much tax you will owe long before the deadline arrives. It also helps you spot problems early, whether that is shrinking margins, rising expenses, or slow-paying customers. Up-to-date records mean fewer surprises and much less scrambling when it is time to file.

Step 2: Track deductible expenses

Every legitimate business expense reduces your taxable income, but only if it is recorded properly. Keeping track of expenses throughout the year ensures you do not miss deductions that could lower your tax bill. It also makes your tax return more accurate and easier to prepare. When receipts and invoices are organized, you spend less time searching for paperwork and more time making informed decisions about your business.

Step 3: Estimate your tax early

One of the best ways to avoid stress at tax time is to estimate what you will owe well in advance. An accountant or bookkeeping software can help you project your tax bill based on your current income and expenses. Knowing this number early gives you time to set aside money, adjust spending, or explore funding options if needed. It turns a looming deadline into something you can plan for instead of fear.

Step 4: Review your cash flow

Your tax bill is only one piece of the financial picture. You also need to look at payroll, rent, inventory, and other obligations that come due around the same time. Reviewing your cash flow helps you see whether paying CRA will create a squeeze. If it will, you have time to make adjustments, speed up collections, or look for financing instead of being forced into last-minute decisions.

Step 5: File and pay on time

When everything is organized ahead of time, filing becomes much easier and far less stressful. Paying on time avoids interest and penalties, and it keeps your CRA account in good standing. That matters if you ever need flexibility or support in the future. Staying on schedule is one of the simplest ways to protect both your business and your peace of mind.

Turning Tax Deadlines into Financial Planning Tools

Tax deadlines are often treated like something to survive rather than something to use. In reality, they are some of the most valuable financial checkpoints in your business calendar. Each deadline tells you something important about your cash flow, your profitability, and how well your business is absorbing its obligations.

When you know when taxes are due, you can plan for them the same way you plan for rent, payroll, and inventory. You can decide when to collect receivables, how much to set aside, and whether a large payment will affect other priorities. Instead of reacting when a deadline arrives, you are making intentional decisions ahead of time.

This shift in mindset turns tax season into a tool. It helps you see where your business is strong, where it is stretched, and what adjustments will keep things running smoothly.

From Tax Deadlines to Financial Confidence

Even with careful planning, there are times when a tax bill arrives at an awkward moment. A big client may have paid late, or expenses may have come in higher than expected. That does not mean your business is failing. It means your cash flow and your tax timing are out of sync.

Merchant Growth works with Canadian small businesses to bridge that gap. By providing fast, flexible funding designed around how small businesses actually operate, Merchant Growth helps you meet CRA deadlines, avoid penalties and interest, and keep your operations running without disruption.

It is not about covering a tax bill. It is about protecting the stability of your business while you continue to grow.